October 2018 Vol. 73 No. 10

Features

Utility & Communications Construction Update

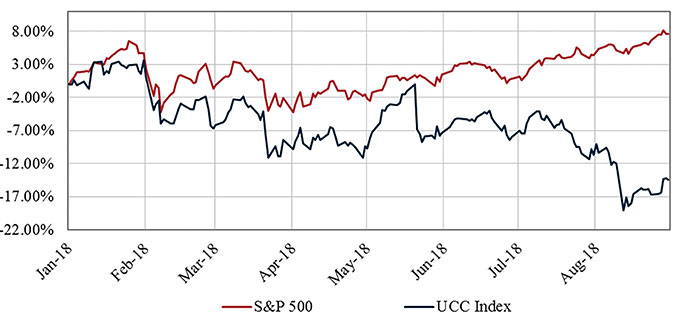

The Utility & Communications Construction (UCC) Index underwent another update as the Granite acquisition of Layne Christensen was approved during the past quarter. Per the three-year (Figure 1), one-year period (Figure 2) and year-to-date (Figure 3) Index, the market is viewing the growth prospects of select UCC Index companies differently.

The UCC Index year-to-date is negative and down significantly compared to the S&P 500, which is near 8-percent growth. The decline is related to the lowered expectations of investors in communications construction due to the timing of 5G fiber implementation, the change in guidance for both Dycom and Mastec, and margin compression attributed to the cost of labor in the construction markets.

The trend observed in the last UCC Update has reversed. Dycom, Mastec and other communications contractors experienced a substantial pullback in valuation because they were unable to provide the earnings growth that the stock analysts were looking for. Because the underlying requirements for 5G and the fundamentals for the utility and communications industry remain strong, we would expect the companies to regain traction as work moves out of engineering.

For most companies in the power and gas distribution markets, growth is strong and expected to continue. Those with exposure to midstream transmission have experienced some challenges due to the permitting and approval process associated with putting pipelines into service. For example, the Atlantic Coast Pipeline has gone through various issues with regulators, permitting and land procurement that have impacted the contractors performing work on the line.

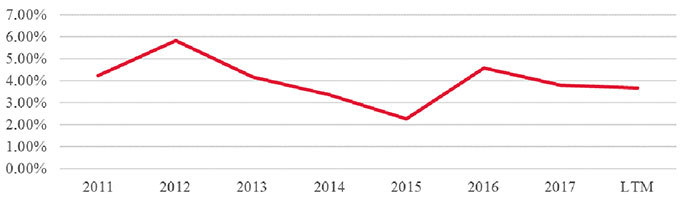

Rather than look at the most-recent operating performance, this quarter we dove into the return on equity (RoE) and underlying drivers of the metric – return on assets (RoA) and leverage. By evaluating RoE with a Dupont Analysis, it’s easy to understand why a company may be viewed as risky by the market and viewed more favorably while doing similar work.

RoE measures the return on one’s equity investment in a company and can be broken into distinct elements that illustrate what drives the metric. Mastec and Dycom have historically high RoE, while companies like Quanta, MDU or Granite have a more muted return. The ability of a company to effectively utilize its assets and the amount of debt involved in financing a company have a large impact on return. Figure 5 provides the average RoA along with annual individual performance.

RoA is an efficiency measurement that determines how effectively a company utilizes its assets. The higher the metric, the better a company is performing.

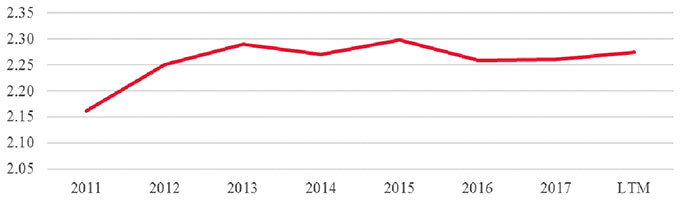

The RoA for companies in the UCCI is compact and the out-performers are not tied to a specific end-market. In 2017, Goldfield, Mastec, Dycom, Primoris and Quanta were the leaders and generated the highest net income with the assets on their balance sheet. RoA provides insight into companies operating efficiently, but does not provide much insight into the discrepancy in RoE among the UCCI companies. Figure 6 provides the average leverage ratio and individual metrics.

The leverage ratio, or equity multiplier, indicates whether a company finances the purchase of assets through debt or equity. The higher the ratio, the more debt that is on the balance sheet. This ratio multiplies the performance (good or bad) and significantly impacts RoE. Since the market also views companies with large amounts of debt as riskier, there will be a much wider range in how the company may be valued.

Communications companies are much more comfortable with higher leverage and this explains the strong RoE from Mastec and Dycom. Companies that have more exposure to large projects are less likely to use as much leverage – Quanta, Granite, Matrix Services and Goldfield are among these. There is lower RoE, but if the market turns they are less exposed to risk factors that could create negative returns.

The summer months were punctuated with significant private equity interest in the utility and communications construction industry. First, ORIX Capital Partners acquired Peak Utility Services Group from CIVC. Investing from its Japanese parent’s balance sheet, ORIX’s entry into the industry represents a new, well-capitalized competitor.

Hooper Corporation expanded operations in July to enter the gas distribution vertical market with the acquisition of Premier Energy Services. This represents a strategic growth path that could allow the company to expand utility services across its customer base.

Lastly, PowerTeam Services was sold by Kelso to Clayton, Dubilier & Rice (CDR), another international capital provider that sees long-term growth opportunity in construction and maintenance of infrastructure. CDR’s interest bodes well for the health of the industry and the potential for private equity to grow as an exit alternative in the underground segment.

Comments