April 2017 Vol. 72 No. 4

Features

Utility & Communications Construction Business Update

EDITOR’S NOTE: The past 25 years has seen many changes in the underground utilities universe. Technology advances, regulatory activity and environmental requirements have dictated major alterations in the way companies are managed. Rating as one of the foremost changes is the evolution of the business model for contractors and utilities. Roll-ups, mergers and strategic acquisitions in the face of boom/bust markets have altered the way contractors and utilities do business. To keep pace with the shifting business of underground, Underground Construction has partnered with the industry’s leading economic consulting company, FMI, to provide quarterly updates on market activities.

The year 2016 provided positive results for the utility and communication construction sectors. Focus on U.S. infrastructure is at historic levels, profitability has improved and valuations have risen. The transmission and distribution of power and gas continue to receive increased investment, water and sewer investment is on the rise and the fiber market continues build-out to meet user demand. Thus, stock prices for the utility and communications construction segment have performed very well. We have produced an index of the publicly traded players with underground construction operations across the energy and communications segments to review historical activity and current expectations.

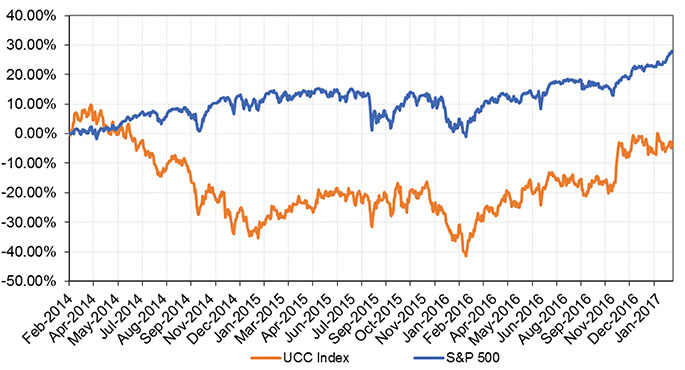

The Utility & Communications Construction Index (UCC Index) presented below presents the stock performance of the sector’s publicly traded stocks over a 10-year period (Figure 1).

The segment was a darling of Wall Street during the residential construction boom, and then benefited from the rise of oil prices and transmission construction into 2014. Because a significant number of the publicly traded companies in the index were involved in construction of crude oil pipelines, or have customers that were impacted by the downturn, the UCC Index companies experienced a depression in stock price that began to rebound in February of 2016.

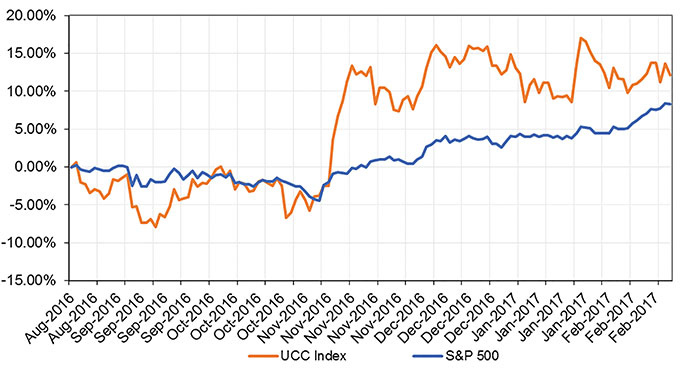

Figure 2 shows the performance for the UCCI since February relative to the S&P 500. This chart highlights the link to oil pricing and the reduction in private pipeline transmission opportunities, even as investor-owned utilities increased their capital budgets. The turnaround in February 2016 related to increased oil prices and then again in November with the “Trump Bump” is stark.

Figure 3 further highlights the impact that the election had on expectations for the UCC Index companies. Pricing has remained consistent since the election, while the rest of the market has seen improvement. Further improvements will require the infrastructure program promises to be realized through legislation and executive action.

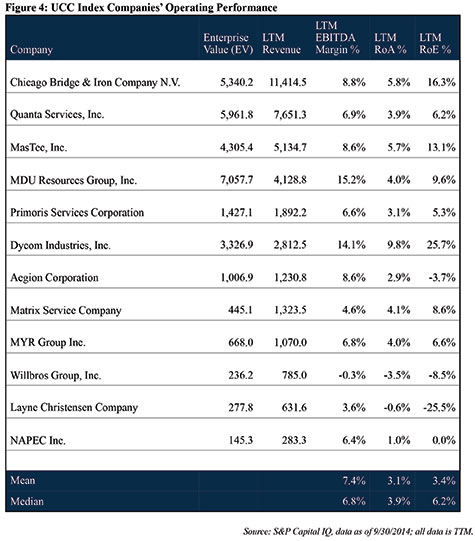

The companies in the UCC Index with exposure to oil felt the squeeze from customers and experienced margin compression over the past three years, which impacted the public market’s valuation of these companies. In contrast, the companies performing work for communications customers saw their margins and profitability metrics improve. The expectation for 2017 is that improved contracts and project opportunities will facilitate increased margin and profitability metrics across the UCC Index companies.

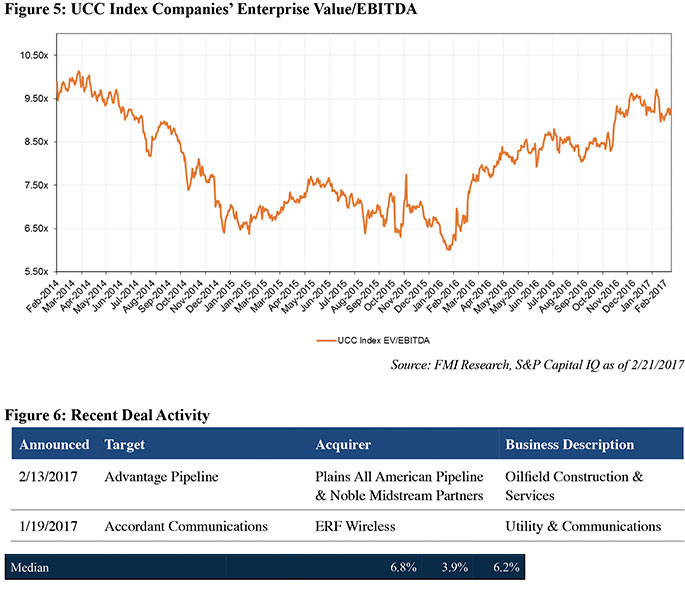

Many of the UCC Index companies put their merger and acquisition (M&A) plans on hold in recent years as they focused on operational improvement and debt reduction. Almost all the players have a well-defined acquisition program, but because of the relatively high Enterprise Value to EBITDA calculation (a measure of valuation that minimizes the impact of taxes and capital decisions) acquisitions have been limited. Figure 5 illustrates where UCC Index companies are trading based on this metric.

Because of the demand for infrastructure repair on distribution systems and the demand-driven requirement for communication infrastructure throughout the United States, we expect investment in companies performing this work to increase. Multiple private equity and family office funds are actively soliciting opportunities to invest in the infrastructure opportunity. The prospects are strong because of the need within the United States for the construction, repair and replacement of vital infrastructure.

Comments