July 2024 Vol. 79 No. 7

Features

Utility & communications construction update shows strong market

By Daniel Shumate, Managing Director, FMI Capital Advisors Inc.

Across the underground utility infrastructure segment, companies are performing quite well in the power, gas distribution, and water and wastewater construction segments. Strong investment by investor-owned utilities, the federal government, states and municipalities led to quality project opportunities that brought significant growth to the contractors serving those markets.

The one group that has experienced challenges in the first half of 2024 are the businesses installing or maintaining communication infrastructure.

After all-time highs for capital investment in 2022 at about $83.5 billion across key publicly traded companies, a retrenchment occurred in 2023. Those companies’ investment plans for 2024 are expected to remain consistent, but not grow at the historic pace of 2022.

In addition, delays in BEAD fund deployment have created additional delays in the deployment of fiber and wireless infrastructure. Demand for maintenance and installation services should increase as the BEAD investment comes online and product prices in the segment moderate, but this may not occur until the second half of 2024 or early 2025.

During the second quarter, a significant addition to the UCC Index companies occurred because of the successful IPO of Centuri Holdings. After the investment by Carl Icahn in Southwest Gas (the investor-owned utility that held Centuri), the divestment of Centuri from Southwest Gas was on the horizon, due to Icahn’s investment thesis.

The company performed well in initial trading and is down slightly in the market, primarily due to the departure of the CEO William Fehrman, to lead American Electric Power. Centuri is one of the largest power and gas distribution companies in the United States and Canada, and the success in early trading bodes well for privately held companies eying the public markets as an exit option.

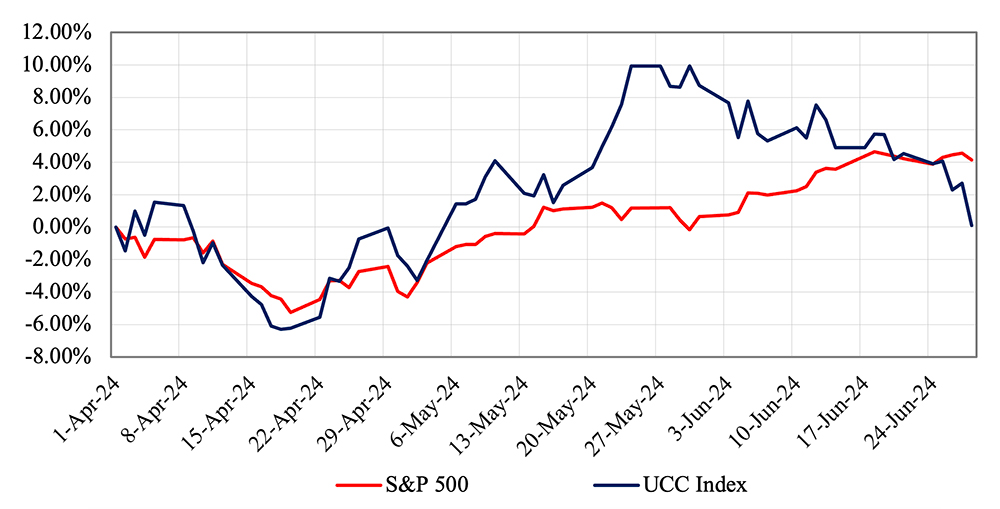

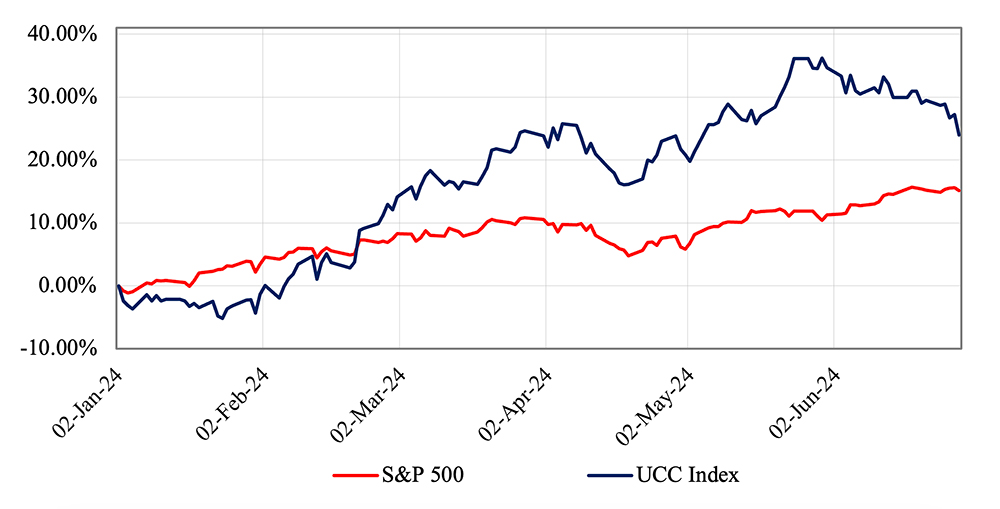

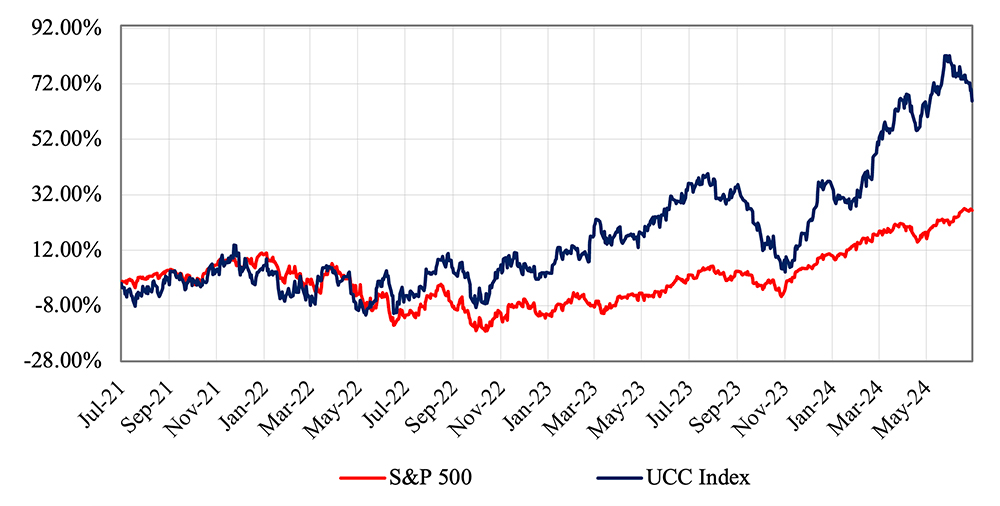

The Utility & Communications Construction Index presented below shows the performance of the sector’s publicly traded stocks for the past three months (Figure 2), year-to-date (Figure 3), and for the past three years (Figure 4).

The S&P 500 has performed well over the past three months and is currently up 15.1 percent year-to-date. This is the first quarter in almost three years where the S&P 500 has outpaced the performance of the UCCI. Growth related to artificial intelligence and companies in the technology sector have surpassed growth rates for the UCCI companies.

The S&P 500 increased healthily as inflation has moderated (though is still above acceptable levels for the Federal Reserve). Expectations for rate cuts in the second half of the year will likely keep valuations high unless there is a notable change in the Federal Reserve’s outlook.

The performance of the UCCI companies over the past three years has been nothing short of remarkable. The UCCI companies’ price has grown 65.9 percent in that period compared to 26.4 percent for the S&P 500. The strong investment by both investor-owned utilities and federal legislation led to strong growth and profitability for these companies. As the IIJA and other legislation is deployed, continued growth at comparable levels to address the nation’s infrastructure will require increased investment by utilities and communication companies.

Companies in the UCCI have grown valuations and maintained consistent performance despite labor challenges and inflation pressures. The double-digit growth by several companies in the industry illustrates the impact of the funding on the industry, as well as the opportunity inherent to the energy transition. As the industry continues to address needs for repairing existing infrastructure, while building resilient power infrastructure for the future, the underground construction segment will remain resilient.

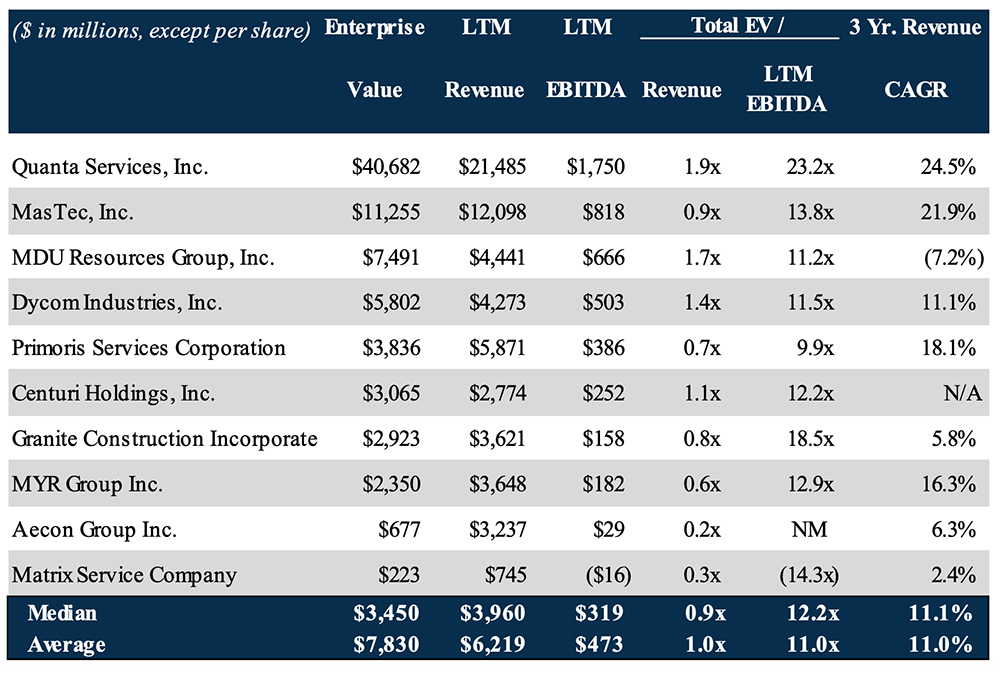

Several transactions occurred during the quarter that continue to mold the shape of the broader industry. PIKE recently added to its engineering capabilities with the acquisition of United’s power delivery group. GridTek Utility Services also was acquired in the quarter and will likely continue to seek acquisitions in the power segment nationally. Other acquirers remain active with both Asplundh and Quanta completing transactions in the quarter, as well.

As companies (both public and private) have grown accustomed to the current interest rate environment, the gap between what a seller is looking for and what a buyer views as acceptable has narrowed. We expect the second half of the year to experience increased M&A activity, as growth in the industry has been strong and investors look toward stable acquisition opportunities.

Comments