February 2019 Vol. 74 No. 2

Features

22nd Annual Municipal Sewer/Water Infrastructure Survey

By Robert Carpenter | Editor-in-Chief

As underground sewer and water personnel look to the near-term outlook for infrastructure construction and rehabilitation markets, financial implications are varied: up, down and somewhere in-between. But, while this information is always elusive by nature, overall market indicators are actually consistent in leaning towards enhanced spending programs in 2019.

In fact, this is the strongest across-the-board projections that the industry has experienced in many years, with every category showing growth. The 22nd Annual Municipal Sewer and Water Infrastructure Survey & Forecast, conducted by Underground Construction magazine in October and November of 2018, queried municipal personnel about a variety of important subjects, among them projected spending for 2019.

The survey results revealed stronger budgets for many cities. While still very cautious, municipal personnel appear to believe that a prolonged, stronger economy – combined with encouraging developments at the state and congressional levels – would support increased spending.

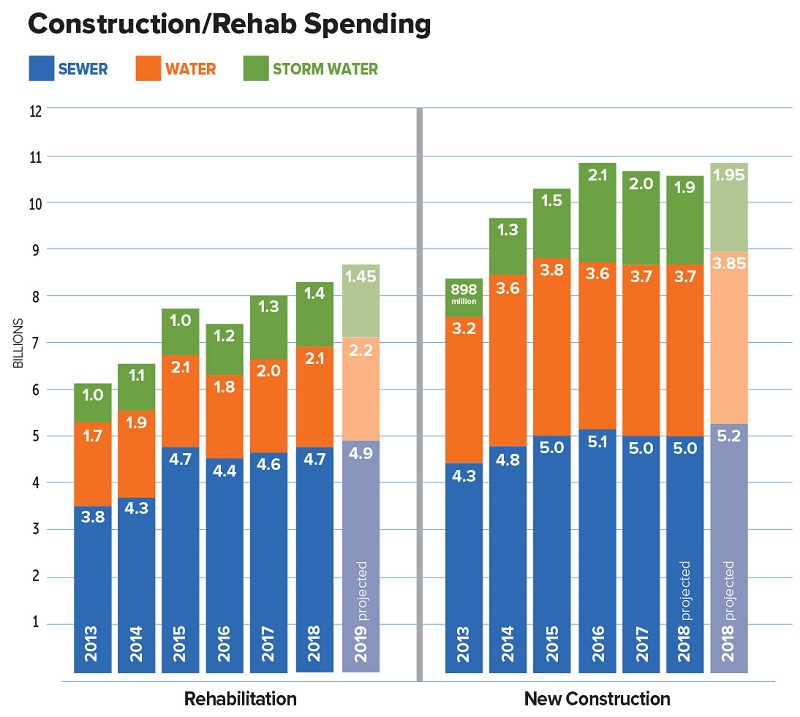

New installation of sewer infrastructure is projected to increase by 3.7 percent in 2019 to $5.4 billion, with a 3.9 percent increase ($3.85 billion) for water construction. Rehabilitation continues to outpace new construction in its growth curve.

Sewer rehab is projected at a 4.1 percent growth in 2019, or $4.9 billion, with water getting a 4.5 percent ($2.2 billion) spending boost. All totaled, that equals projected spending plans for sewer, water and stormwater piping infrastructure of $19.75 billion in the United States for 2019, representing an overall increase of 3.7 percent.

The survey polled U.S. municipalities about their top concerns and issues, 2019 infrastructure spending plans, and working relationships with consulting engineers and contractors. Th is exclusive annual study also provides detailed insight of America’s cities with information and perspectives on industry topics and technology. The survey reflects only information regarding sewer, water and stormwater piping infrastructure and does not include figures or data on pumping stations, treatment plants, etc.

Respondents ranged in size from rural communities of less than 500, to mid-sized cities, as well as a representative sampling of the nation’s largest cities.

Funding sources

The bulk of funding in recent years has been coming from local or state sources, with limited aid from federal programs. However, there are signs that more funding may be slowly developing at the national level. Several national government-related positive developments regarding sewer/water infrastructure funding have been steadily evolving into fruition.

Infrastructure received a boost in October when President Trump signed the America’s Water Infrastructure Act (AWIA) which enjoyed rare, strong bipartisan support. The law had several provisions supporting, such as a new Drinking Water System Infrastructure Resilience and Sustainability program. Th is grant program offers competitive grants to small or disadvantaged drinking water systems that wish to construct projects that increase the resilience of their infrastructure to a range of natural hazards.

After the Democrats took over the House of Representatives in November, Sen. Chuck Schumer felt empowered to send a letter to President Trump advocating pro-climate change policies through investments in water, waste and sewer infrastructure. Apparently, Trump’s staff was receptive to the proposal.

The Environmental Protection Agency’s (EPA) 2019 budget has not been set due to the government shut-down still in effect at press time. However, it appears likely that the State Revolving Funds (SRFs) will get increases in fiscal 2019 once final appropriations are passed.

The Water Infrastructure Finance and Innovation Act (WIFIA) finally received funding and is expected to increase to $75 million in 2019. While the SRFs provide revolving loans to the states and localities, WIFIA provides credit assistance for large projects with the expected FY 2019 appropriation leading to about $8 billion in loan capacity.

Further, a major infrastructure investment plan, much ballyhooed by both Republicans and Democrats in recent elections, may finally emerge in 2019. Several bills are under development and passing infrastructure legislation is a goal of both political parties, so it has a reasonable chance of gaining bi-partisan support. Of course, just how much funding would be specifically devoted to sewer and water remains the big question.

Indeed, when asked what the most important issue is facing cities for 2019, funding was the overwhelming concern expressed by a large majority of survey respondents. “We desperately need clarity in our funding options,” stressed a municipal official for a large Northeast city. “We’ve had too many years of budgeting high and spending low.” Said this West Coast respondent, “Lack of adequate funding makes maintaining our systems at effective levels almost impossible. There is no room for growth.”

Added an upper Midwest municipal director, “We need to be able to plan and build for the future as our city is growing. But we’re very concerned about upgrading what’s already in the ground first. To do all that takes a lot of money and we don’t see that being available without some help.”

Active EPA

To complicate matters further, the EPA remains active in pursuing cities, large and small, that are out of compliance with environmental standards and regulations. In 2019, we’ll probably see at least two major cities go under a consent decree program, and a plethora of other municipalities are currently in the negotiation stage with the EPA. For cities, of course, this represents another immediate funding crisis, yet presents somewhat of a work bonanza for consulting engineers and contractors.

Regardless of possible boosts in funding appropriations, whether from national or state levels, the need for expanded spending exists and the local citizenry is increasingly vocal in concerns for dependable and efficient sewer or water systems to be in place. The Flint, Mich., contamination disaster clearly elevated public awareness for potable water systems – especially if any lead pipes are involved.

Various industry associations have also steadily raised public awareness of the disastrous condition of sewer and stormwater systems. It’s taken years and unfortunate disaster, but progress has been made on the public relations front – enough so that elected officials must seriously consider infrastructure issues. About 40 percent of respondents said their 2019 budgets were greater than in 2018, while 22 percent have smaller budgets. About 38 percent expect their budgets to be about the same.

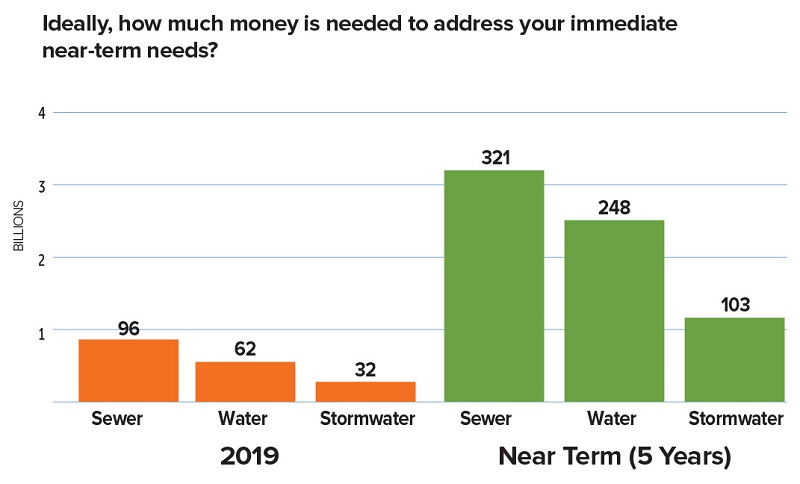

When asked for a ballpark estimate of how much money was needed to update, expand or rehabilitate their infrastructure, respondents didn’t pull punches. “This would be a dream – to have adequate funds to bring our system up to date,” sighed this Southeast muni spokesperson. “But I don’t think we’ll ever have funds available to accomplish that.”

Respondents estimated they would need $96 billion for sewer, $62 billion for water and $32 billion for stormwater to adequately meet their needs in 2019. In the long term, survey participants anticipate needing more than $600 billion.

Workforce, other issues

In addition to funding issues, several other topics were frequently cited by survey respondents, including ongoing workforce issues. “Hiring and retaining qualified employees” is an ongoing struggle, according to an official from this Southwest city.

“We’re losing tremendous legacy knowledge and skills without finding adequate replacements,” complained a Northeast municipal employee.

Getting “qualified operators to replace workers who will be retiring,” is also an ongoing problem said this Mid-Atlantic representative.

Observed a respondent from the Pacific Northwest, “we have a hard time attracting new, young talent to the municipal field.”

Other issues mentioned were problems in achieving “completion of very complex construction projects on-time and on-budget,” reported this Southwest respondent. “New regulations and the EPA/DEQ,” was also cited as an ongoing issue by this municipal representative from the upper Midwest.

Regulations and “dealing with the EPA” was repeated frequently by several other survey respondents. Municipalities rated several broad categories as to how much of an impact each had on their operations. As discussed earlier, funding remained the number-one concern, with 80 percent of the respondents. Regulations and the EPA were cited by 70 percent of the respondents; hiring qualified employees was mentioned by 40 percent; safety concerns by 40 percent; and community relations by 30 percent.

Rate increases for user fees have historically been very hard to push through local governing agencies. However, desperate times require desperate measures and city governments find themselves without options – they must raise their rates in order to keep systems functioning. Survey respondents reported an average of 2.9 years between rate hikes, down from 3.1 a year ago.

Asset management continues to gain traction with America’s cities. More than 44 percent of America’s cities report having a program fully in place, while 34 percent have a program in development. Roughly 22 percent have no plans to implement an underground asset management program at this time.

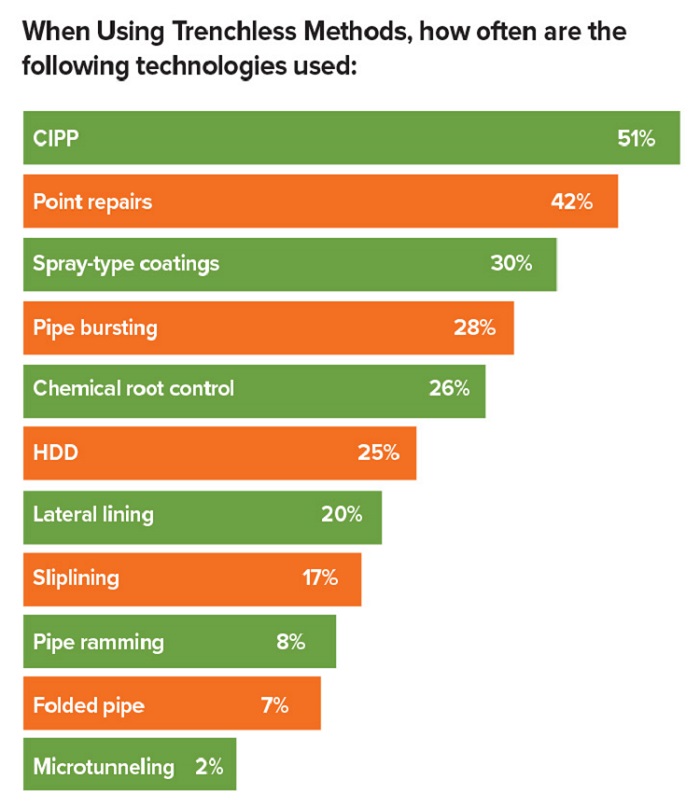

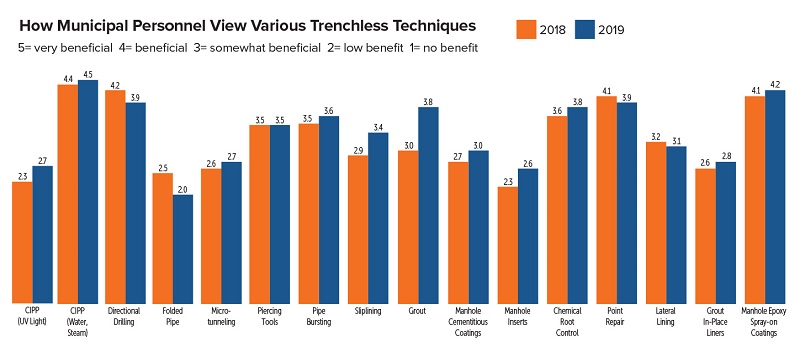

As mentioned earlier, trenchless rehabilitation is still experiencing a solid growth curve. More and more products are entering the market place or existing products are getting more refined. Expertise in various technologies by both municipal and contractor personnel have also acted to improve the value of rehabilitation. Cities estimate that roughly 56 percent of the pipe repairs today are performed with trenchless rehab.

Another interesting side note is that about 50 percent of those surveyed commented that they prefer to use trenchless methods when feasible, while 30 percent said it didn’t matter to them, and 20 percent still prefer open-cut methods.

“For us, trenchless versus open-cut is a site-by-site decision,” said a Midwest muni manager. “Cost is an issue,” said a Mid-Atlantic respondent.

“Depends on the location and situation,” pointed out this respondent from the upper Midwest. “Trenchless works very well in the right circumstance.”

Rating engineers, contractors

The survey asked municipal personnel to rate the consulting engineering community. An overall rating was a composite from four categories: quality of work, timely project completion, fair pricing and dependability, based on a scale of 1 (worst) to 5 (best). The consulting engineer’s score for 2019 was 3.9 compared to 3.7 in 2018. That represents another big jump in confidence levels for engineers, who for several years were languishing at 3.0 or lower. But over the past few surveys, consultants’ ratings have steadily climbed.

When asked what are the most important values they look for in engineering firms, quality was the near-unanimous choice cited by municipal mangers. Other areas included “understanding of new technology” (80 percent of respondents), “cost” (70 percent of respondents), and “productive relationships with contractors” (25 percent).

Municipal personnel were also asked to suggest how engineers could do a better job for sewer and water agencies. A municipal employee from the Pacific North-west said, “communication in all aspects of the project from design, bidding, construction and close out,” is extremely important.

Another survey respondent from the Midwest advised that engineers should “understand the parameter of the project. Offer alternate solutions and give alternate bids that incorporate a life cycle alternate/analysis.”

This Midwest municipal manager advised that engineers should always “be transparent and truthful.”

Yet another comment that was suggested in similar form by several survey respondents, was for engineers to “understand the field side of the business.” A Mountain West city employee complained that “too many consulting engineers rarely get in the field to see technology in use, witness the challenges and problems that crop up.”

Municipal personnel were also asked to rate contractors based on the 1-to-5 scale in the areas of quality work, timely project completions, price and dependability. Unfortunately for contractors, their composite score dropped for the second year in a row, down to 3.7 from 3.9.

“Timely completion of work is a big issue for us,” stressed a Southeast municipal manager.

A respondent from the Mid-Atlantic region added that contractors should “devote more time to the job instead of rushing at the last minute to get work completed.”

Advised this municipal respondent from the Midwest, “Bid jobs correctly, don’t underbid to get in the door, then expect extras to make up for the real cost.”

Another common complaint about contractors was reluctance to branch out into other construction methods that could improve execution of a project. “Contractors need to be willing to work with new products, follow specifications and do quality work,” said this Northeast respondent.

From the desert Southwest, a municipal employee observed that “too many contractors are comfortable with their backhoes and don’t want to try something else.”

Added a respondent from the Southeast, “We like for contractors to advise and work with us on alternative construction methods. Sometimes that’s not the answer, but it should always be explored.”

Comments