July 2018 No. 73 Vol. 7

Features

Utility & Communications Construction Update

Daniel Shumate | Director, FMI Capital Advisors Inc.

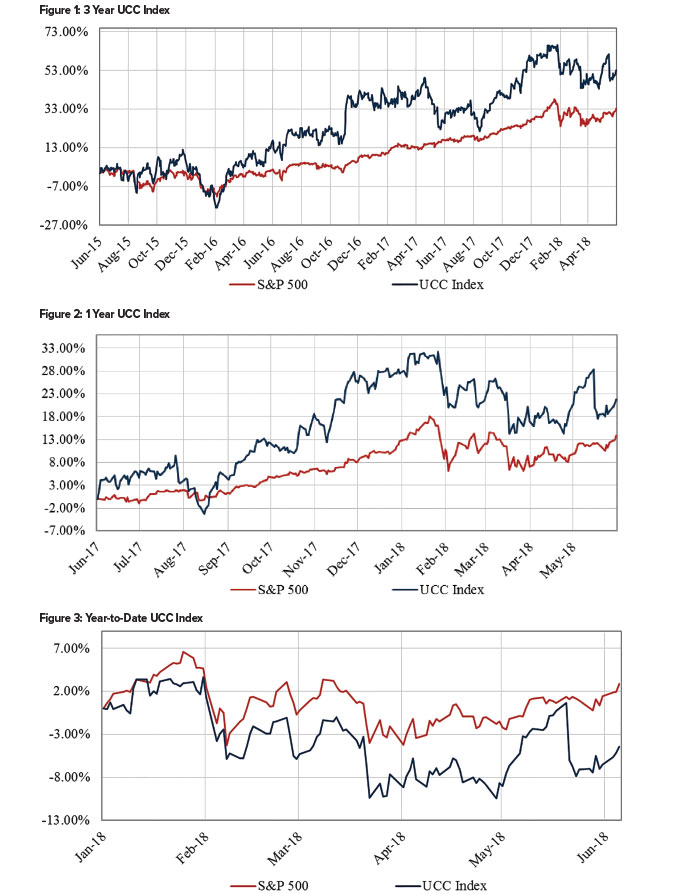

The Utility & Communications Construction Index (UCC Index), updated to exclude Willbros Group due to its acquisition, presents the performance of the sector’s publicly traded stocks over a three-year period (Figure 1) one-year period (Figure 2) and year-to-date (Figure 3). Notably, the revised UCC Index has performed better than the S&P 500 over a three-year period and over the last 12 months, as infrastructure construction and repair have been strong drivers of the sector. Year-to-date, we see a decline, as earnings have lagged and trade concerns, specifically related to steel pipelines, have affected the segment.

There is a notable divergence in power, versus communication, industries in the underground over the last six months. Dycom, MasTec and other communication contractors are seeing significant valuation increases, as the communication market invests substantially in fiber to the home and fiber to businesses.

In addition, the 5G rollout by major wireless providers requires increased fiber backbone in major U.S. cities and is driving the communication contractors’ business. The power and gas markets are steady and do not have the same growth expectations. The return on equity provided by utility commissions, power load growth, regulatory pressure and the Canadian economy are concerns relative to the communications industry, which is experiencing rapid build-up.

As we constantly seek to gauge where the industry is in an investment cycle, we often monitor the best indication of industry health – the ability to produce cash flow. Free cash flow is the amount of cash that can be distributed to shareholders, after the necessary investment to sustain earnings in the coming year (i.e. investment in the equipment and machinery to perform on the next year’s contracts). In industries with rapid growth, we expect free cash flow to decline, as investment increases for future opportunities.

In mature industries, we expect the value to remain constant. Looking at the last five years, the total free cash flow of UCC companies has been variable, but has not grown significantly (Figure 4). Because the economy and industry have been improving, we would expect a greater increase in cash flow. However, margin pressure, due to a tight labor environment and the investment in future growth, has been impacting cash flow since 2015.

The most interesting metric we analyzed was the change in valuation over the past five years. The industry dipped to valuation in late 2014 and early 2015 of less than 20.0x EV/FCF. The metric spiked in 2016 on anticipation of infrastructure funding from the federal government, and has settled near historical norms of ~30.0x free cash flow. Thus, the market suggests we are in a mid-point of the cycle, with expectations for the public companies at the historical average.

The companies in the UCC Index on average have seen slight margin contraction (Figure 5) due to various activities in the first quarter of 2018. The biggest factor was the weather that impacted the ability of companies to achieve results similar to the prior year. The communications companies continue to lead the pack in return and, most notably, market valuation (enterprise value). Companies with exposure to the power markets in Florida, Houston and the Caribbean experienced profit improvements, as remaining construction efforts in the wake of the fall hurricanes were completed.

UCC Index companies again are the story of M&A during the second quarter of 2018 (Figure 6). The primary deal that was quashed is the acquisition of AECON by CCCC. The Canadian government decided to guard the construction of critical infrastructure (similar to the United States), rather than allow the sale to one of the primary Chinese construction companies. Granite’s acquisition of Layne Christensen became more interesting, as some primary shareholders continue to put up a fight for increased value for the company. The proxy process is still ongoing, but will be decided soon.

The newest acquisition is the decision by Primoris to prevent the bankruptcy of Willbros by acquiring the company. With a purchase price of approximately $100 million, it’s an all-cash transaction. Primoris financed the acquisition through existing facilities so that the team could move quickly.

This acquisition establishes Primoris in the electrical infrastructure market and expands its field service offerings. It also increases the company’s footprint into the Southeast and its large project capabilities. Management at Primoris will have difficult decisions in the coming months, wrestling with the profitable divisions that sustained the company, while preventing the losses that brought Willbros to an unstable position.

Power engineering, construction and maintenance were the themes for the remaining transactions. Forbes Brothers expanded its U.S. presence with the acquisition of Titan Electric. Midas Utilities increased its offerings in the Southeast and Intren acquired Miller Construction, expanding its woman-owned business enterprise. Gryphon Investors in San Francisco also invested in the utility and industrial construction industry by acquiring Shermco from the GFI Energy team at a strong valuation.

Comments