January 2023 Vol. 78 No. 1

Features

NA Pipeline Construction Outlook

Jeff Awalt | Executive Editor

(UI) — Seldom has a new year arrived with the degree of supply and demand uncertainty facing global energy markets at the start of 2023.

Months of soaring oil and natural gas prices gave way in late 2022 as oil demand projections softened on recessionary fears and Europe’s months-long buying spree filled its natural gas storage levels to near capacity. Counterintuitively, Brent prices fell further in December even as the OPEC+ cartel announced new supply cuts and Europe’s ban on Russian oil imports forced Moscow to reroute supplies.

That was partly because the OPEC+ cuts turned out to be harsher on paper than in practice. The announced 2 MMbpd – roughly 2 percent of global supply – turned out to be more like 1 MMbpd, as some cartel members struggled to make quotas. The impact of European price caps on Russian oil and gas, meanwhile, remained questionable as 2022 came to a close.

While 2022’s rollercoaster pricing fell into backwardation before year-end, there were enough contrarian indicators to give December’s bears heartburn.

U.S. shale production, which provided most of the world’s supply growth in recent years, has fallen to a snail’s pace as producers react to higher costs and lower prices. A months-long selloff of U.S. strategic reserves appeared poised for reversal as pricing approached the $70/bbl level that would trigger a refill.

Indications of slowing inflation and an anticipated softening of China’s demand-crushing COVID policies also support projections of tight gas supplies in 2023.

“China’s COVID policy is the most important fundamental factor for global demand in commodities and energy in 2023, as its demand softness due to lockdowns in 2022 was a key safety valve for oil, gas and coal markets, while Europe scrambled to replace Russian energy,” Dan Klein, head of Energy Pathways at S&P Global Commodity Insights, said in December.

“With another year of vaccinations and growing frustrations with lockdowns domestically in China,” Klein said, “restrictions will likely ease somewhat in 2023 and imports of fossil fuels can be expected to increase again.”

Natural gas impacts

Activity in global pipeline construction markets is predominantly driven by natural gas, with Europe eyeing new sources to replace Russian supplies and the Asia-Pacific region continuing to expand its import, transmission and distribution infrastructure, led by India and China.

Even before 2022 and Russia’s invasion of Ukraine, global energy markets were strained as demand returned faster than supply. Even if commodity supply/demand balances loosen more than expected in 2023, S&P’s Klein notes that almost all markets will require “another year or more of recalibration before inventories, balances and prices return to a more sustainable equilibrium.”

Moreover, despite Europe’s success at building gas stocks ahead of the 2022-23 winter, that feat may prove to be more daunting in the months ahead as the continent faces a full year with scarcely a trickle of Russian gas. Planning and construction of liquefaction and regasification facilities, along with supporting natural gas pipeline infrastructure, is moving ahead, but nearly all of the new LNG supply will come online after 2023.

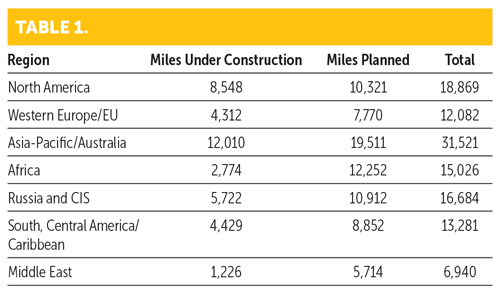

These trends were reflected in Underground Infrastructure/Pipeline & Gas Journal’s annual analysis of pipeline construction activity, which found 114,403 miles of pipelines either planned or under construction worldwide at the start of 2023. Of those, 86 percent are natural gas projects and 14 percent are liquids pipelines. Projects still in the planning, engineering and design phases represent 75,332 miles of the total, while 39,071 miles are in various stages of construction.

The combined figures reveal a 10.7 percent increase in total mileage compared with the 113,305 miles of pipelines that were planned or under construction in our 2022 survey.

Total mileage increased in four of seven regions, including gains of more than 50 percent in both Europe and Asia-Pacific, while North America, Africa and South and Central America posted declines.

Total mileage of pipelines planned and under construction across all regions at the start of 2023 includes Africa, 15,026 (-9.9 percent); Asia-Pacific, 31,521 (+50.6 percent); Western Europe, 12,082 (+57.5 percent); Russia/CIS, 16,684 (+11.6 percent); South/Central America and Caribbean, 13,281 (-18.2 percent); North America, 18,869 (-13.8 percent); and Middle East, 6,940 (+39.2 percent).

North America outlook

Pipeline mileage either under construction or set to kick off in 2023 equals 8,548 miles with another 10,321 being planned.

U.S. LNG has been a critical source of Europe’s supply and is projected to meet more of the EU’s natural gas demand in the future. Export capacity is currently maxed out, but more natural gas pipeline and LNG export capacity is being added through numerous projects to help meet growing international demand.

With pipeline takeaway capacity bottlenecked in the gas-rich Marcellus Shale, the Haynesville Basin of Northeast Texas and Louisiana and the Permian Basin of West Texas and New Mexico are stepping up to meet most of the surging European demand. Canada is also moving forward with natural gas pipeline and LNG export projects, but with cargoes primarily aimed at Asian markets.

Both the Haynesville and Permian can deliver natural gas to LNG facilities on the U.S. Gulf Coast via intrastate pipelines, potentially streamlining permitting and construction. As a predominantly dry gas basin, activity in the Haynesville shale has historically been limited by low natural gas prices, but its fortunes have reversed with higher prices and ever-increasing demand forecasts tied to nearby LNG plants.

Haynesville production growth has been made possible with expanded pipeline takeaway capacity, including Midcoast Energy’s CJ Express pipeline, which entered service in April 2021, and Enterprise Products Partners’ Gillis Lateral pipeline. The related expansion of Enterprise’s Acadian Haynesville Extension also entered service in December 2021.

Those three projects added 1.3 Bcf/d of takeaway capacity from the Haynesville area, raising its total estimated takeaway capacity to 15.9 Bcf/d, according to PointLogic. That figure suggests excess takeaway capacity out of the Haynesville is at or below 900,000 Mcf/d, or about 7 percent of total capacity.

In response, Energy Transfer started construction of the 1.65 Bcf/d Gulf Run pipeline to move gas from the Louisiana Haynesville to the Gulf Coast. That project, which Energy Transfer gained via its acquisition of Enable Midstream in December 2021, is backed by a 20-year agreement with the $10 billion Golden Pass LNG export plant now under construction in Texas by QatarEnergy (70 percent) and Exxon Mobil (30 percent).

Energy Transfer completed the trunk line of Gulf Run before the close of 2022 and was conducting an open season for deliveries beginning Jan. 1. Co-CEO Marshall McCrea told analysts last year that the Dallas-based company also was making progress toward potential FID for its own LNG export project at Lake Charles, Louisiana.

Quicker with intrastate

As pipeline operators look toward intrastate pipelines as the fastest path to expansion, two distinct corridors are developing for egress from the Haynesville, with pipelines from the Louisiana side aimed at LNG facilities on the Louisiana coast and proposed projects from the Texas Haynesville targeting Texas LNG exports, along with increasing Permian volumes.

Williams announced in late June that it has reached a final investment decision (FID) to build its proposed Louisiana Energy Gateway (LEG) project to gather natural gas produced in the Haynesville. The project is set to move 1.8 Bcf/d of gas to several Gulf Coast markets, including its Transco gas pipe from Texas to the U.S. Northeast, industrial consumers and LNG export plants.

Williams said LEG, which is expected to enter service in late 2024, will enable it to pursue additional market access projects, including development of carbon capture and storage infrastructure. Kinder Morgan has said it also is evaluating a project to link the Texas Haynesville with LNG export points on the Texas side of the border.

Additional North American LNG export capacity will be added with the expected 2023 startup of the $17 billion LNG Canada Export Terminal, which is currently under construction in Kitimat, British Columbia. It will have a production capacity of 14 mtpa from the first two trains, with the potential to expand to four trains.

LNG Canada, which will supply Asian markets, will get its natural gas supply via the 48-inch, 416-mile Coastal Gaslink natural gas pipeline now under construction by TC Energy. It will be the first major transmission pipeline to move natural gas across the Canadian Rockies to the British Columbia coast. The pipeline was approaching 65 percent completion, as its June project update.

Canada is also looking at LNG export expansion on its east coast to expand capacity to Europe, but Environment Minister Steven Guilbeault said existing natural gas infrastructure would only be able to supply one of two proposed options: an LNG facility in New Brunswick by Spain’s Repsol or in Nova Scotia by Pieridae Energy.

Guilbeault, who said the idea of constructing new gas pipelines to supply east coast export facilities is not “very realistic,” told Reuters that Repsol is “probably the fastest project that could be deployed, because it requires minimal permitting,” with a pipeline already in place.

In Mexico, New Fortress agreed with Comisión Federal de Electricidad (CFE) in July to increase its supply of natural gas to multiple CFE power generation facilities in Baja California Sur and the development of a new LNG hub off the Gulf of Mexico coast at Altamira, Tamaulipas, with multiple FLNG units of 1.4 MTPA each. CFE will supply natural gas via existing pipelines to two FLNG units.

Comments