April 2021 Vol. 76 No. 4

Features

2021 Utility & Communications Construction Update

By Daniel Shumate, Managing Director, FMI Capital Advisors Inc.

As we contrast March of 2020 to March of 2021, the changes are truly unprecedented. Beginning in March of 2020, over 22 million would lose jobs within two months, most of the American economy was put on life support, and we knew very little about the virus that would upend our daily lives.

Fast forward to 2021 where Americans are beginning to have access to vaccines, the virus is on the wane, and the prospect for meaningful infrastructure support is probable and the picture is much more stable. Substantial investment is expected to occur in both urban and rural power markets, as well as communication markets over the coming 12 months. I talk often about the opportunities and expected investment (which remain high), but we also want to make sure that at a high point for stock valuations and optimism , we pay attention to risks, as well.

One risk for those with exposure to oil and gas is the regulation and de-emphasis of all fossil fuel related infrastructure. In the markets that are most aggressive, we have seen calls for “no new gas service hook-ups” while in other regions, the environmental pressures for permitting have limited normal activity.

In addition, we anticipate a continued decline in U.S. oil production despite the recent price increases due to challenges put in place by the Biden administration. This will impact our power generation markets meaningfully – with the switch to electric heat and electric cars, the demand for power in the United States is expected to rise rapidly and generating capacity will likely be unable to keep up without the use of fossil fuels.

The second risk could come from the bond markets, as the treasury is pushing more debt into the marketplace. If the infrastructure bill is as advertised, at nearly $2.0 trillion, then in the past 18 months, we would have appropriated over $8 trillion in stimulus. It is almost impossible to put that number into context, but in less than one year, the United States will have seen gross federal debt grow over 18 percent (representing ~$84,000 per American).

This can impact the infrastructure market in many ways, but a couple of examples include: if bond yields rise meaningfully, then the cost to finance projects increases and the amount of work that can be completed goes down. Alternately, if the cost to finance U.S. debt increases meaningfully, then we can see higher taxes and market -limited government spending in future years.

The third risk that we are monitoring is the single-family market. Currently, limited housing supply and very low mortgage rates have caused prices to increase significantly, creating wealth for homeowners. However, 5.2 percent of mortgages (2.7 million) are in forbearance due to governmental limitations on foreclosures that represents $547 billion in unpaid principal.

This artificial decrease in supply and expected decline in demand, as people return to the office and are in less need of additional rooms to work and play, will likely see supply increase meaningfully. FMI also anticipates rates to increase due to inflation pressures in late 2021, early 2022. This will decrease the buying power of the buyers and put downward pressure on the prices we are seeing today.

While this primarily impacts the new construction segments focused on residential markets, those developments, new hook-ups and highways that require relocation of utilities impact the underground market.

UCCI performance & updates

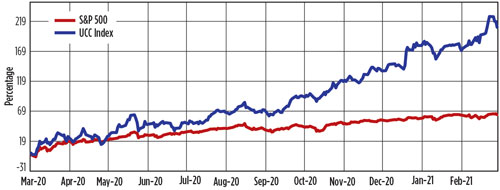

The Utility & Communications Construction Index (UCCI) presented below presents the stock performance of the sector’s publicly traded stocks over the past quarter and the past year. The UCC Index will no longer include The Goldfield Corporation, as it has been acquired by First Reserve Corporation in a take-private transaction in the final quarter of 2020.

The first quarter of 2021 has been incredible relative to the broader market. The UCCI is up 30 percent versus 6 percent for the S&P 500. Expectations for a large infrastructure bill that moves through Congress to budget reconciliation is the expectation. We also have experienced meaningful capital investment projections from utility, communication and government entities expecting a low-rate environment with ample federal support.

The one-year performance of the UCCI is up 207 percent over a grisly point as the pandemic had startled markets and the sell-off was in full swing. For the investor that bought at that point, the UCCI generated returns substantially above the S&P 500 (increasing 63 percent over the same period).

Mergers & acquisitions

Due to the liquidity in the marketplace and the anticipation for increases in spending on power, communication and renewable infrastructure, deal activity is robust. In the public markets, we would anticipate additional shelf offerings (like Primoris and Orbital Energy Group) to increase available funds for acquisition activity. In the private markets, we expect continued consolidation and diversification of services by incumbents that historically relied on the oil and gas markets.

The first quarter was comprised primarily of add-ons to existing platforms except for the majority interest in Pike taken by Lindsay Goldberg. The Pike family will remain significant shareholders in the business, but an additional private equity group entered the infrastructure services arena.

Comments