June 2019 Vol.74 No. 6

Features

UC Exclusive: 21st Annual Horizontal Directional Drilling Survey

HDD Prosperity is Tempered with Challenges

Robert Carpenter | Editor-in-Chief

In 2019, horizontal directional drilling (HDD) is again riding high, based upon a series of strong markets. However, the question asked by many is how long will the robust HDD market last? The better question, perhaps, is how sustainable are the aggressive growth patterns of the fiber, gas distribution, electric and energy pipelines construction markets? HDD prosperity is directly tied to all these markets yet continues to find healthy niches not even considered in the past.

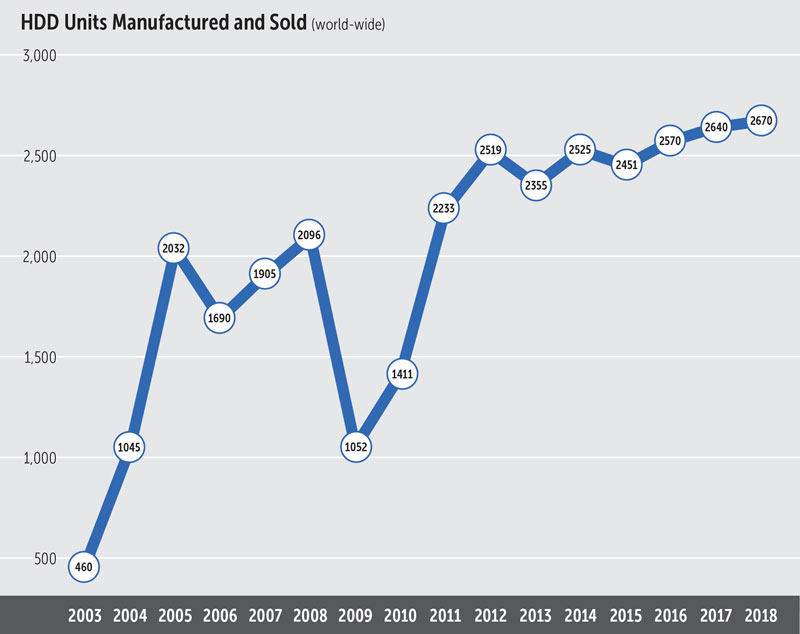

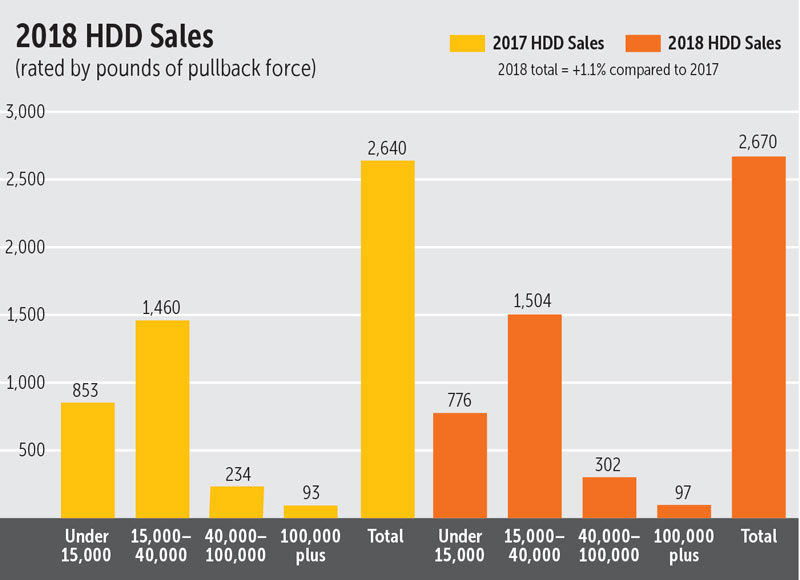

In 2018, the 2,670 drilling rigs (all sizes) sold was the most since the fiber boom days of 2000, when almost 4,000 units were purchased. While, most likely, HDD will not approach those lofty levels any time soon, the current rig sale volumes do demonstrate a strong, diverse market, and 2019 levels should come close to, or perhaps even exceed, 2018 levels.

The 21th Annual Underground Construction HDD Survey reveals the strength, versatility and growth that the HDD market has sustained for many years. This exclusive industry research was conducted during March and April. It surveyed contractors and some utilities that actively own and operate HDD units to enable a statistical portrayal of the market.

Fiber

There is no doubt, especially for the small- to mid-sized rig markets, that the reemergence of fiber installations over the past 10 years as the leading force in the telecommunications industry has contributed mightily to the current boom. The use of HDD technology goes hand-in-glove with underground telecom installations. The build-out of fiber-to-the-home, fiber-to-the-premises—fiber-to-anywhere—just refuses to slow down. A wide variety of experts struggle to definitively predict when the fiber build-out will slow, with guesses ranging from 3 to 7 years.

Just as fiber work paused slightly a couple of years ago and Google decided it no longer wanted to be in the construction market, several major carriers, including AT&T, finally launched their fiber installation growth programs, and work quickly ramped back up. Also, smaller- to mid-size carriers continue to expand their plants and bring fiber to communities. Recently, Google has started showing signs it may reenter the fiber infrastructure market.

Further, smaller cities are increasingly building out their own networks, refusing to wait for a “down-the-road” timeline from big companies. To top things off, the next wave of mobile phone service, 5G, is in full force. This is bringing more construction work for telecom contractors, most of whom rely heavily upon HDD as their primary construction tool for underground installations. And finally, rural areas are beginning to become active targets for fiber expansion.

Ironically, it was the lack of fiber-to-the-premises which played a pivotal role in the turn-of-the-century crash. Long-builds of fiber networks across America’s landscape brought promise of speed and bandwidth to the fledgling internet services. Fiber was going to put communications at light-speed and bring unheard-of economic, educational and social opportunities to homes and communities across the country. To paraphrase a famous movie line, “Build it and they will come” was the attitude of the late ‘90s as more and more fiber backbones spread around the country. The problem was, they didn’t come.

Private customers were not prepared for the expensive jump to fiber service, especially when it came time to pay for installations at their homes. In most areas, fiber backbones were miles away, making it economically unfeasible for homeowners to import the service to their houses. The telecoms themselves were also not prepared at that time to absorb the financial burden of fiber-to-the-premises. There were no workable plans to reach a critical mass of subscribers, both residential and commercial, that could justify the massive cross-country network construction activities. Subsequently, without enough cash flow to support the backbone buildouts, the market crashed—and HDD along with it.

“We had jumped big into installing fiber,” recalled an established contractor in the Midwest. “When the bottom dropped out, we were left with a lot of idle HDD rigs and equipment. At that time, we didn’t know how to use HDD for anything else and those other markets were underdeveloped anyway. Fortunately, we were able to fall back on our traditional utility work and we survived.”

Diversification

Today, the market dynamic is much different. Over the past 18 years, HDD has been embraced broadly by virtually every market involved in underground installations. While telecom is still a leading driver and user of HDD equipment and services, the same can be said to a lesser degree for gas and electric distribution, oil and gas pipelines, water distribution/transmission and even sewer force mains.

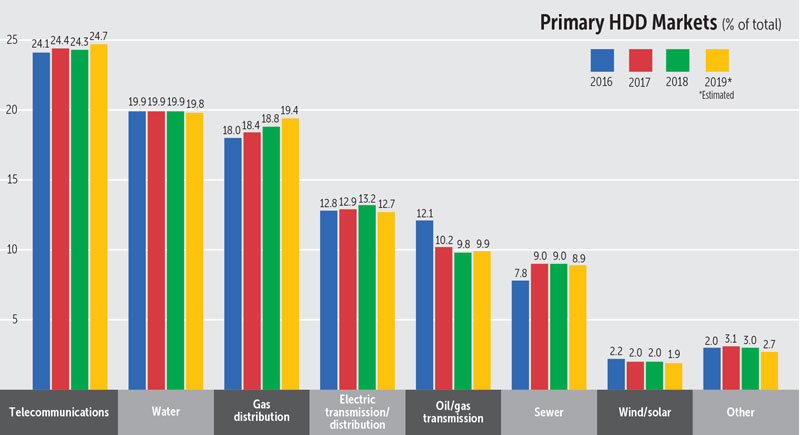

The survey revealed that while telecom still represents the largest market segment for HDD applications at 24.7 percent, following closely are water installations (19.8 percent) and gas distribution (19.4 percent). Even with the rush to construct alternative power systems focused on wind and solar, underground utilities are needed to connect the systems to power grids. That, of course, means trenching and frequently, directional drilling. Roughly 2.7 percent of the market is consumed by eclectic, yet profitable, uses of HDD.

For 2019, contractors expect HDD to be involved in roughly 47 percent of their projects, with that number growing to 51 percent in five years. The average contractor performing at least some kind of HDD work owns an average of 4.1 mini rigs, 1.9 mid-sized rigs and one large or jumbo rig.

In 2018, about 38 percent of contractors executed up to $1 million of HDD work, 41 percent performed $1 to $5 million, 10 percent had HDD work worth between $5 and $10 million, and 7.1 percent had completed projects in excess of $10 million.

While most of the survey respondents believe HDD will continue to be an expanding market for the short term, at least, one West Coast respondent cautions that 2020 is a presidential election year, and that could impact the construction markets.

As with any strong market segment, opportunists emerge that can, even unintentionally, create major ripples throughout industry, often creating negative impacts. HDD is no exception. “The market is getting saturated with new companies, and that is causing depressed pricing,” complained a Midwest contractor. Added another contractor respondent, “The huge boom has resulted in too many inexperienced start-ups.” Another respondent stresses that the influx of new contractors continues to create “pricing pressures.”

Other issues

But it’s not just competition for the dollar that concerns many of the survey respondents—it’s how some contractors perform their work. “Some of these inexperienced companies have really created problems for us,” related a Southeast contractor. “They don’t know how to properly bid projects. And what’s worse, they don’t know how to do a good job.”

Said this respondent from the Southwest, “The new guys are giving HDD a black eye.” Another contractor from the Southeast added, “I’m worried that somebody is going to get seriously hurt.”

As underground utility installations of all types continue to increase in scope, due to advantages in life cycle costs, minimal downtime and safety concerns, not unexpectedly, rights-of-way (ROW) are getting crowded. “We have difficulty due to so many utilities being in the ground now and no place to run,” said this respondent from the Southwest. “Our biggest challenge is congestion of the ROW and fly-by-night contractors,” said a Mid-Atlantic contractor.

A related issue expressed by several respondents was accurate locating. “Locating, potholing and tracking are all major challenges for us,” related this Northeast U.S. contractor. Added a contractor from the Northwest, “we can’t afford to rely on contract locators, so we pothole aggressively on all our jobs. Of course, that increases costs and no one wants to pay for that!”

Disposal of drilling fluid remains an issue for many contractors across the country and was cited frequently in the survey comments. “It’s only going to get worse,” lamented this respondent from the Rocky Mountain region. “We work in several states and mud disposal is becoming an issue with not only state regulators, but counties and cities, as well. It is a very expensive problem.”

Mud/fluids mixing, cleaning, recycling and reclaiming equipment have steadily become more refined and effective in recent years. This is a direct response to more diverse and intense demands from contractors as their mud disposal challenges become much greater with increased regulation. “Anything manufacturers can do to help with our mud needs and issues is greatly appreciated,” emphasized a Southwest contractor.

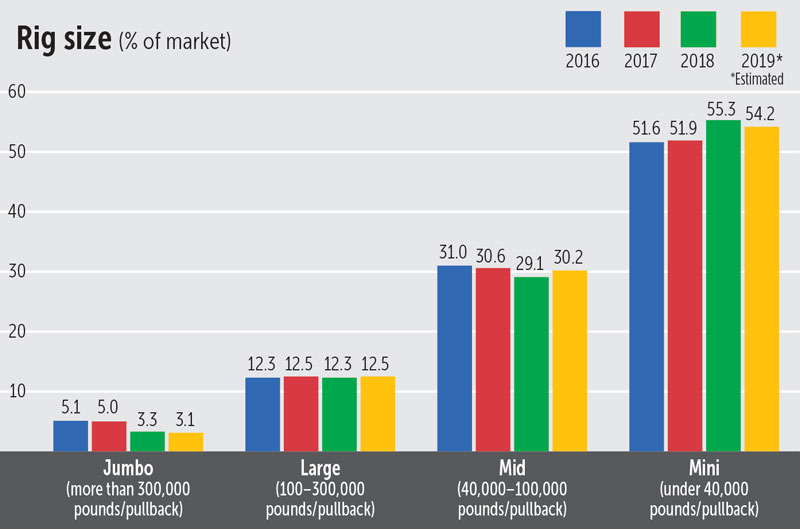

Also trending for HDD markets is the addition of mid-sized rigs to the fleets of typically smaller rig contractors. With the ease of use, enhanced rock capabilities and boost in power of modern rigs, more and more contractors have discovered they can dramatically expand their range of opportunities to complement their standard project fare.

Many contractors are also considering not only adding mid-sized rigs, but expanding into large rig sizes as well. As HDD has become a regular staple of underground markets, application diversity continues to open doors for contractors. Indeed, the survey reflected a substantial jump in sales for 2018 of rigs in the mid (40.000–100,000 pounds of pullback force) and greater than 100,000 pounds (pullback) categories.

Getting younger

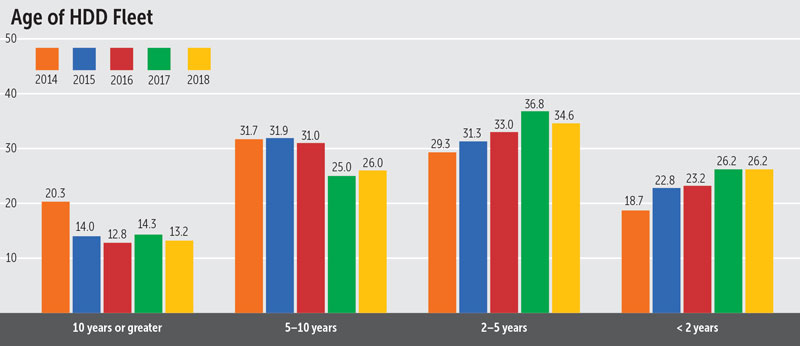

The average age of a contractor’s HDD rig fleet got younger again in 2018, down to 13.2 percent for rigs 10 years or older, compared to 14.3 percent in 2017. A large part of that trend reflects the steady influx of new contractors into the market combined with the expansion of fleets by established contractors trying to keep up with demand. About 26 percent of rigs are five to 10 years old, 34.6 percent are 2 to 5 years old and 26.2 percent of all rigs in use today were purchased within the past two years.

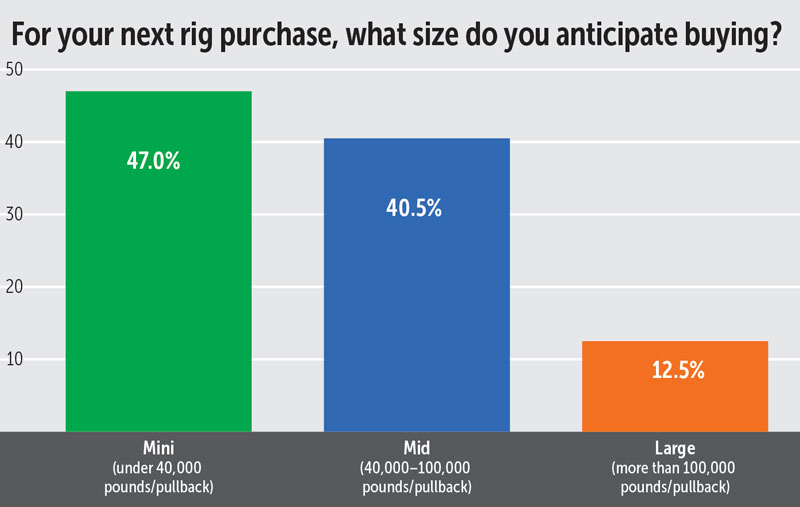

That same scenario of expanding HDD fleets, combined with new entrants into the market, continues to give rise to a thriving used rig industry. For 2019, 65 percent of the respondents have bought used units. In 2019, it is expected that 54.2 percent of used purchases will be smaller rigs (under 40,000 pounds of pullback force), 34.1 percent of respondents plan to buy medium-sized used rigs (40,000 to 100,000 pounds of pullback), and 11.7 percent would be interested in purchasing a large rig (greater than 100,000 pounds of pullback).

Original equipment manufacturers’ (OEM) role in the HDD tooling and drill pipe sectors is vital to many contractors. About 43.6 percent of downhole tooling and 48.1 percent of drill pipe is purchased from OEMs.

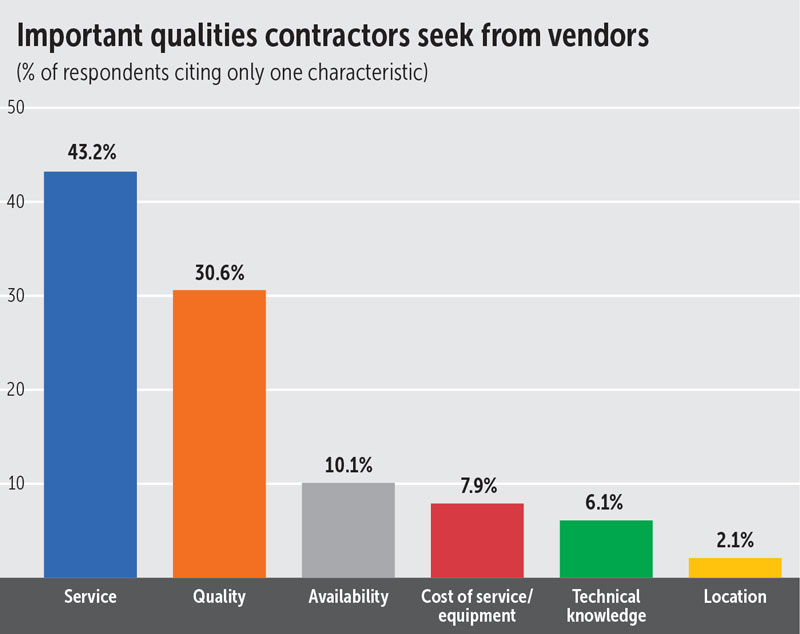

The survey also asked about the most important qualities contractors seek from the manufacturer and supplier partners. “Service” repeats again as the most coveted attribute, as it was cited by 43.2 percent of respondents, followed by quality at 30.6 percent. Surprisingly, cost of equipment/service was only cited by about 8 percent of contractors.

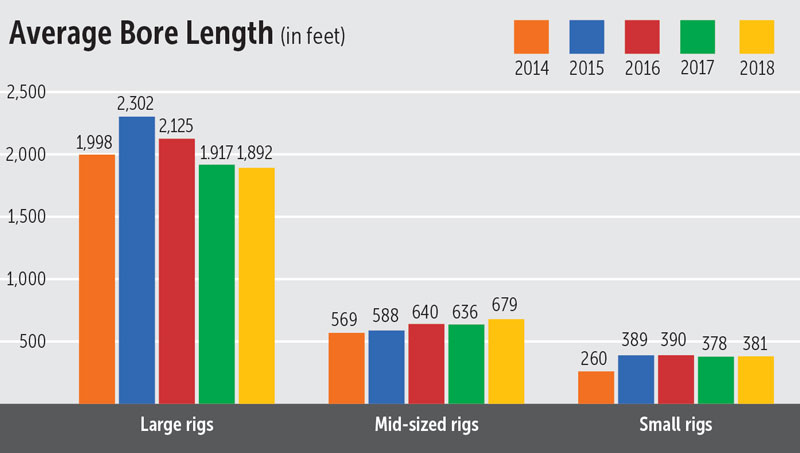

Bore lengths didn’t change much, year-over-year. A typical drill through average soils was 1,892 feet for large rigs, 679 feet for mid-sized rigs and 381 feet for small rigs.

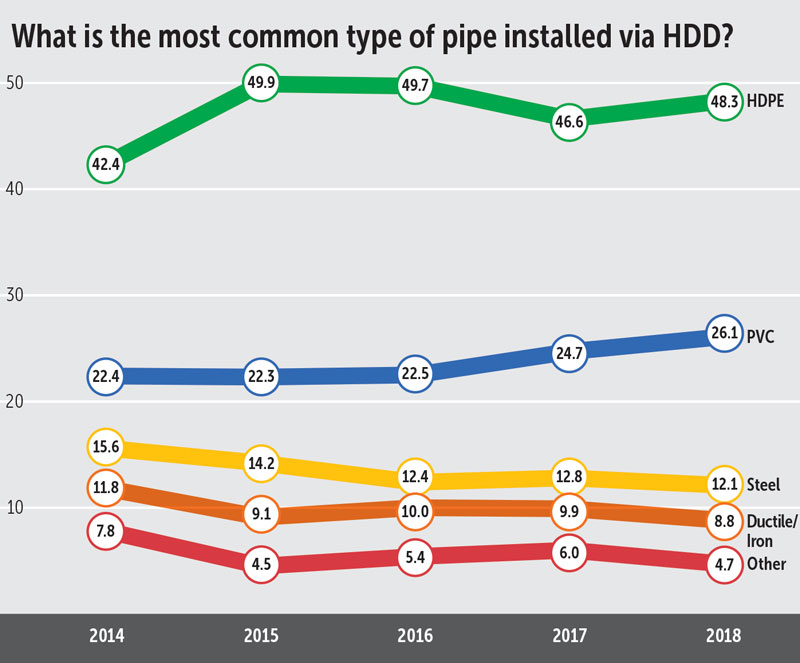

The most common pipe installed via HDD remains HDPE, with a 48.3 percent market share, while PVC remains strongly entrenched in second place at 26.1 percent. •

Comments