July 2019 Vol.74 No. 7

Features

Utility & Communications Construction Update

Daniel Shumate | Director, FMI Capital Advisors Inc.

Mixed revenue and profitability results marked the second quarter of 2019 for the utility and communications industry, particularly among the publicly traded members of the Utility & Communications Construction Index (UCCI). Quanta Services continues to increase both its revenue and profitability. UCCI companies are near all-time highs of revenue, but experienced declines in profit margins during the quarter.

Near-term growth opportunities remain strong, with investor-owned utility and telecommunication company capital expenditures expected to increase year-over-year. The primary drivers of this spend are similar: aging infrastructure that requires repair or replacement, reliance on the contractor to provide labor to supplement utility workforce, and demand-driven spending on fiber infrastructure.

Two factors influenced the challenging operating environment during the opening months of 2019. Extreme winter weather resulted in a decline of construction jobs during February, and record rainfall impacted both March and April, either slowing footage per day or sidelining work in the underground entirely. The result was a decline in revenue with an increase in costs, impacting the companies within the UCCI. Trenchless construction, pumps, construction mats, shoring and other methods promote safety and allow the underground construction company to continue to operate. However, the work is much-less efficient and profitability suffers.

The second factor impacting the UCCI companies is a trend toward “megaprojects” that can have an outsized impact on profitability, even as revenue increases. Megaprojects increased to 33 percent of total construction starts in 2018 and the trend continued, with $718 billion in megaprojects being awarded in the first half of the year.

The trend is expected to continue over the next 10 years to address industrial and infrastructure challenges across the country. First, there are the projects that are fixed price. Here, the contractor is most at risk and can enjoy either great benefit or loss, depending on performance. However, the cost of labor and materials has increased rapidly over the past two years, so projects that were bid in 2018 can experience margin fade as the jobs occur over multiple years.

Another common type of contract is a unit-priced blanket contract. These are typically more favorable to the contractor because total risk is broken into units of work, and there are usually escalators within the contract to handle significant price increases. However, the rate at which labor and material costs have increased has outpaced the escalators. If a contractor fails to anticipate the rate at which prices will increase in the bidding of these unit contracts, then the ability to perform well on those units is severely impacted.

The result is a contract that requires the contractor to perform work at tight margins or at a loss over an extended period, and can weigh heavily on contractor performance. As large blanket contracts and megaprojects continue to influence the infrastructure landscape, strong communication in the bidding phase, healthy rate modifiers and clear authority chains to modify contracts during construction are a few ways that can improve contractor profitability and lower total job cost.

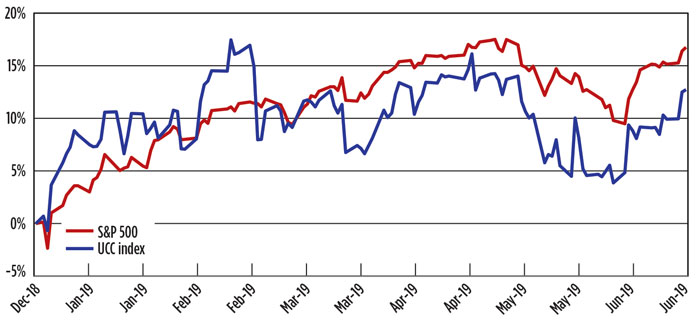

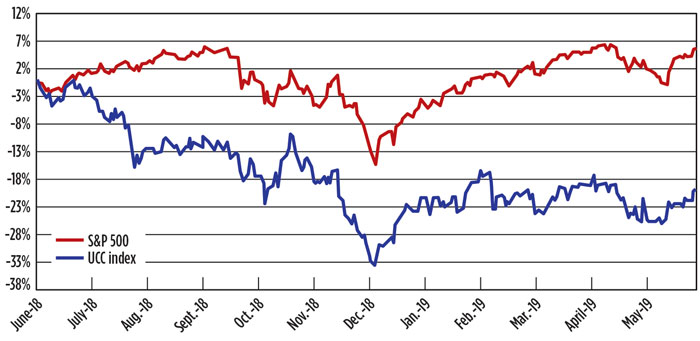

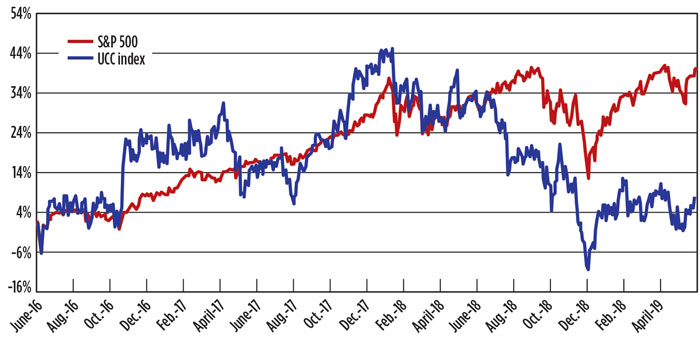

The UCCI presented below presents the performance of the sector’s publicly traded stocks year-to-date (Figure 1), the past one year (Figure 2) and the past three years (Figure 3).

Year-to-date (YTD) performance is average relative to the performance of the S&P 500. February 2019 represented a high point for the UCCI due to expectations for an infrastructure bill and rising oil prices. Oil prices have not increased at the rate expected, companies have missed earnings expectations due to weather and cost increases, and the infrastructure bill failed to materialize.

The results are depressed stock prices relative to other segments of the market. Revenue is higher year-over-year for the UCCI companies. However, profitability must continue to improve for the segment to outperform.

UCCI remains more volatile than the S&P 500. There are two primary periods that have influenced the index’s performance relative to the broader market. Figures 2 and 3 illustrate the declining performance of the UCCI, while the S&P 500 continued to rise from June through October of 2018 and then again February through April of 2019. The result is market growth of almost 7 percent over the past 12 months, while UCCI has declined over 20 percent.

The drop in the 2018 UCCI correlates with the decline in oil prices and the recognition that 5G construction rollout was moving slower than expected. In 2019, the decline is much more performance oriented. One of the wettest winters across the country impacted revenue growth alongside increasing labor and material costs.

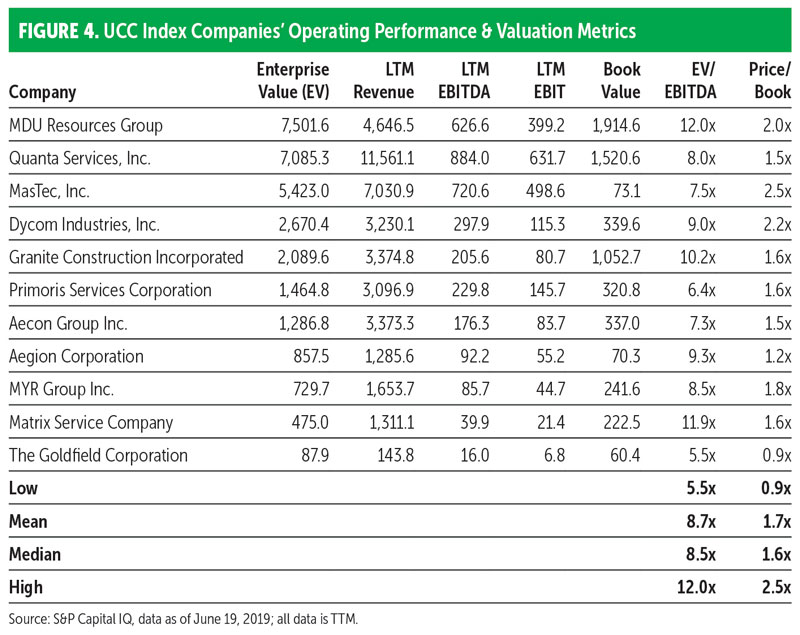

As we look at valuation (Figure 4), the worth of companies within UCCI have varied significantly based upon backlog, operating performance and exposure to select end markets. Overall, valuation has increased, but not at the rate of the broader market.

Valuation will be influenced by macroeconomic factors in the next two quarters, as trade discussions in North America and with China play out. In addition, the Federal Reserve has slowed rate increases and could reverse course if the economy slows to boost market activity.

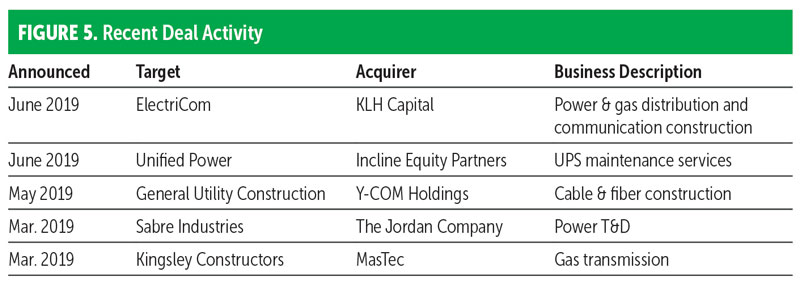

Second-quarter 2019 deal activity (Figure 5) has held steady, as consolidation continues in underground construction and solutions in the gas, power and communication segments. MasTec invested in the gas transmission segment with its acquisition of Kingsley Constructors. This increased its presence in the Permian Basin and capabilities in the midstream market.

Private equity also continues to invest in the underground infrastructure segment. KLH Capital, Incline Equity and The Jordan Company invested in companies performing installation, repair or replacement of power and communication infrastructure. With investment expected to continue, through investor-owned utilities on infrastructure in need of repair and major communication companies on their 5G infrastructure, growth and consolidation in the underground market will remain strong. •

Comments