April 2018 Vol. 73 No. 4

Features

Utility & Communications Construction Update

2017 sustained a stretch run of positive results for the utility and communications construction sectors. While the path to a federal infrastructure bill is still tenuous, investment is occurring at the state level, and investor-owned utilities and private communication companies continue to invest in their systems with capital expenditures reaching historic levels. Profitability among contractors has improved and valuations have risen. Thus, stock prices for the utility and communications construction segment have performed well.

M&A activity has altered the makeup of the index of the publicly traded players that have underground construction operations across the energy and communications segments. The Utility & Communications Construction Index (UCC Index) has been adjusted to exclude NAPEC and Layne Christensen because they are finalizing acquisitions with third parties. In addition, a new company, Granite Construction, has been added to the list because of its current merger agreement with Layne Christensen. While we anticipate this transaction will occur, Littlejohn & Co. (an investor in Layne Christensen) has filed an opposition letter to the current agreement, and the merger could run into issues if investors do not feel they are receiving adequate value.

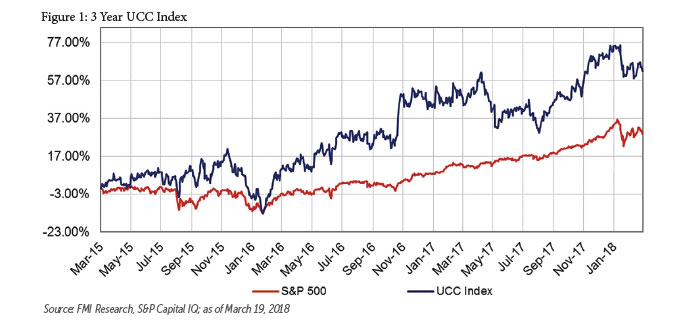

The UCC Index presents the stock performance of the sector’s publicly traded stocks over a three-year period. The segment has performed well relative to the market during this period of heavy investment in U.S. infrastructure. Figure 1’s three-year time frame captures how the industry has operated under the “new normal” of oil at $60 per barrel, since the price stabilized.

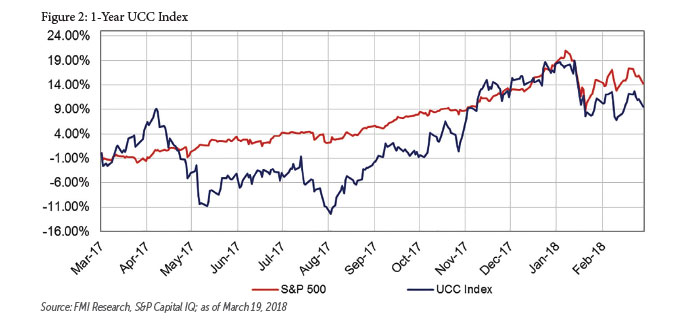

Figure 2 shows the performance for the UCCI over the last 12 months relative to the S&P 500. This chart demonstrates the volatility that is impacting the segment – the most significant of which is the questionable political environment that the industry is operating within. The most important takeaway is that while the S&P 500 has been driven by well-performing, high-tech stocks, utility and communication constructions sectors have kept pace with the market over that time frame.

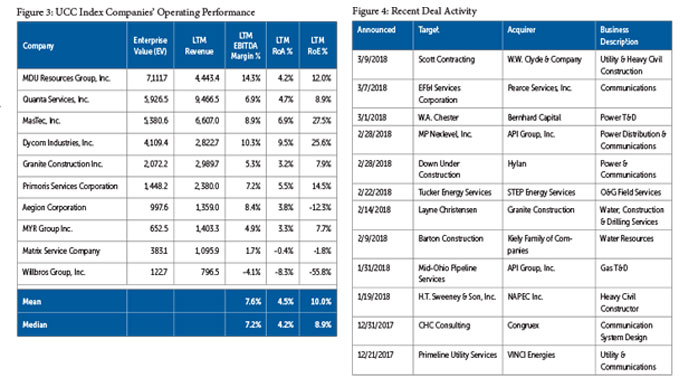

On average, companies in the UCC Index have seen margin expansion over the last 12 months. The only limitation on profitability has been the availability and cost of labor to meet the needs of a demanding customer base. The communications companies have performed very well over the last year. Both Dycom and Mastec recorded improved Return on Asset (RoA) and Equity (RoE) percentages in 2017.

In contrast to 2016, oil and gas and power construction companies also saw their return profitability improve, and EBITDA margins across the industry are strong. The expectation for 2018 is that improved contracts and project opportunities will facilitate increased margin and profitability, subject to material and labor cost challenges as inflation begins to rise.

The UCC Index companies have both participated in and been the target of M&A throughout 2017 The first quarter of 2018 was no different (Figure 4). A large volume of transactions has occurred since the start of the year, driven by improving profits and valuations.

Buyers are seeking companies that can recruit, train and retain employees. They are also striving to capture long-term contracts that have profitable unit price arrangements. Long-term incumbents of the infrastructure segment have well-defined acquisition programs and have stayed disciplined, but new entrants have increased the Enterprise Value to an EBITDA multiple (a measure of valuation that minimizes the impact of taxes and capital decisions) to break in to a profitable and growing segment of the economy. A substantial amount of building capability and revenue has new ownership after the last three months of activity. More than $2 billion in enterprise value has traded during this time. Two significant acquirers have expanded their holdings in the United States: API Group, a privately held holding company based in Minnesota; and VINCI Energies, a French public company that has significant experience as a concessionaire and constructor in Europe. The largest transaction in this time frame is the potential sale of Layne Christensen to Granite Construction. The companies have signed a definitive agreement subject to a number of closing conditions necessary to finalize the sale. If the internal conflict between shareholders in Layne Christensen s resolved, the transaction should close in the second quarter of 2018. The most interesting element of the agreement is the investment by Granite’s management in the water infrastructure market to diversify its heavy highway focus.

Comments