June 2016, Vol. 71 No. 6

Features

18th Annual HDD Survey: Diverse Markets Drive HDD Forward

To say that we are in confusing economic times would be an understatement, not only for the United States but the world in its entirety. The U.S. market confusions result primarily from a mix of political uncertainty, lackluster economic growth and performance, and the collapse of the oil and gas industry.

Fortunately, for several segments of the underground utility construction industry, life is good. Telecommunications construction in particular is surging at levels not seen since the 1990s. The drive to provide fiber-to-the-premises continues to accelerate, driven by an overwhelming consumer and business appetite for bandwidth. In addition to the well-known giants such as AT&T and Google Fiber, telecommunication utilities of all sizes are engaging in massive installation and upgrade programs. In late 2015, communications technology behemoth Ericsson announced plans to essentially become a contractor and facilitate an even faster installation pace for fiber lines. The company claimed it was making this radical move due to customer demand and that the current fiber network build-out was woefully behind schedule.

Other markets in the underground industry are extremely active and vibrant as well, such as gas and electric distribution. The workloads of the water industry, especially in lieu of the recent lead concerns, make new installation of mains a state and national legislative focus.

For those involved in horizontal directional drilling (HDD), these markets represent a perfect match of technology and need. It is a technology segment of the underground infrastructure industry whose upside is virtually infinite.

In this healthy economic environment, telecommunication utilities are particularly motivated, anxious to provide services for growing audiences that have become restless with slower internet speeds or limited bandwidth. This has prompted the aggressive fiber-to-the-premises build-out we’re experiencing now.

This fiber boom differs from the well-documented rise and fall of telecom in the 1990s. Then, utilities were practicing the “build-it and they will come” strategy primarily focused on businesses. The bust started in 2000 due to extensive overbuilding for a telecommunications market place that was still in its infancy. But telecom did mature quickly – and continues to do so – rapidly growing its scope with the broad technological advances requiring massive increases in speed and capacity. HDD has proven consistently that it is an essential element necessary to keep up with the mad pace of construction.

This information and much more are detailed in the 18th Annual Underground Construction HDD Survey of the U.S. market. This exclusive industry research was conducted during March and April and targeted contractors and organizations that actively own and operate HDD drilling units. The number of completed surveys allowed for an accurate statistical portrayal of the market.

As mentioned earlier, gas distribution is going through its own renaissance period. While efforts to replace and upgrade antiquated cast iron pipe continue at a very strong pace – while keeping many businesses extremely busy – demand for new systems is placing additional stresses on contractors and directional drilling specifically.

Challenges

While this sounds like a great time to be an HDD contractor, the market is not without its drawbacks and challenges. A Southeast region contractor pointed out that “the biggest challenge facing the HDD market today is finding qualified, dependable drillers.”

While this sounds like a great time to be an HDD contractor, the market is not without its drawbacks and challenges. A Southeast region contractor pointed out that “the biggest challenge facing the HDD market today is finding qualified, dependable drillers.”

There are efforts being made by several industry groups to make serious attempts to tackle the workforce issue for underground infrastructure. The Distribution Contractors Association has developed an initiative with fresh ideas, relevant data and possible courses of action. The association is hoping this program will be embraced and supported by other industry groups. HDD is certainly a key element of that initiative.

Specifically, for HDD, two leading equipment manufacturers, Vermeer Corp. and Ditch Witch, have launched major programs aimed at helping relieve the void of proper training for HDD operators. These targeted training programs have different approaches but the sponsors are optimistic that their programs will be effective in helping to train effective drillers. The advantage these companies have is working jointly with many dealers scattered around the country, even the world, to support the corporate efforts.

The strong telecom market is having another benefit for contractors. In recent years, telecoms have been notorious for squeezing dollars out of the contractors working for them. Profit margins have been reduced substantially to the point that one small misstep on a project can often mean the difference between profit and loss for a contractor. Telecoms have also been reluctant to accept change orders – even when obviously justified.

The strong telecom market is having another benefit for contractors. In recent years, telecoms have been notorious for squeezing dollars out of the contractors working for them. Profit margins have been reduced substantially to the point that one small misstep on a project can often mean the difference between profit and loss for a contractor. Telecoms have also been reluctant to accept change orders – even when obviously justified.

But as the telecom work grows faster than the number of available contractors, the days of cheap or below-cost work are rapidly coming to an end. Increasingly, contractors are holding their ground on rates as they have plenty of other employment options. “We walked away this year from a company we have been working with quite some time. We had to – they kept wanting us to cut our prices to the point we couldn’t make money,” lamented a contractor from the Southeast. “We were able to do that [walk away] because we had several other companies wanting us to work for them. We’re now working a reasonable price. The company we used to work for has come back to us wanting to renegotiate, but it’s too late.”

For all the HDD work involved in telecom, gas and electric distribution, it generally encompasses mainly small- to mid-size rigs. Larger equipment does have an important and growing role to play in these markets, but the big driver for large rigs has been the oil and gas pipeline construction boom which has slowed dramatically since late 2014. As oil prices dropped from the $90s to the $20s, drilling quickly followed. Plans for major future pipeline projects are frequently being shelved.

For all the HDD work involved in telecom, gas and electric distribution, it generally encompasses mainly small- to mid-size rigs. Larger equipment does have an important and growing role to play in these markets, but the big driver for large rigs has been the oil and gas pipeline construction boom which has slowed dramatically since late 2014. As oil prices dropped from the $90s to the $20s, drilling quickly followed. Plans for major future pipeline projects are frequently being shelved.

Actual pipeline construction has slowed of course, but continued at a fair volume through 2015 and into 2016. Most of the new shale oil and gas wells are located in non-traditional areas where pipelines are rare at best, nonexistent at worse. For owning companies, it was essential to complete projects and continue with some additional construction as there is no effective way to get product to market. Low prices do not support rail or trucking of mass quantities of oil or gas.

Large-rig HDD companies have kept reasonably busy for the past year. Many have had a solid of 2016 to date with ample work line up until later in the year. “We have enough work on the books to keep us pretty busy through most of the third quarter,” said one large rig HDD contractor. “That said, with pipeline construction continuing to slow, we’re concerned about later in the year and into 2017.”

Diversification

Before the oil and gas boom became all-consuming for so many companies, diversification had come to mid-to-large directional drilling. The fiber construction market growth generated substantial need for long crossings or large bundle pull-ins that were best suited for larger rig operations. The electric transmission industry is increasingly feeling the pressure to place the large tower infrastructure with underground cables. While technically feasible, cost is still an issue but there appears to be a strong future ahead for this type of work which generally requires larger rigs to perform.

Another area of expansion for mid-to-large rigs continues to be the water market. Locating and transporting adequate water supplies have municipalities of all sizes scrambling for solutions. Large directional drilling has definitely become a major tool for engineers when designing water transmission projects.

Another area of expansion for mid-to-large rigs continues to be the water market. Locating and transporting adequate water supplies have municipalities of all sizes scrambling for solutions. Large directional drilling has definitely become a major tool for engineers when designing water transmission projects.

A good indicator of the HDD market health is the confidence that survey respondents have for the role drilling currently plays with their work and perhaps even more importantly, how it will impact their market over the next five years. Contractors that actively utilize HDD as part of their equipment toolbox say that HDD accounts for about 52 percent of their work. In 2021, expect that to increase to almost 58 percent.

“I see the long term of HDD only getting more common and open trenching in inner city becoming less,” said a Western state contractor. A Southwest contractor agreed: “I see the near and long-term market to keep increasing. There seems to be localized fiber booms going on and a ton of people flocking to the Google fiber work. But I hope it is not a repeat of the first fiber boom.” A contractor in the Southeast said, said “for us, business has been very good. The market was a bit slow last year but I see us catching up for the next couple of years.”

But strong markets are also bringing an influx of new contractors into the HDD arena – and that can create its own set of issues, according to several survey respondents.

Complained one Northeast contractor, “Companies are able to purchase used equipment at a fair price, but they really don’t know how to operate the equipment, and then underbid those that do know how to operate equipment properly.” Commented a Midwest contractor, “More companies are getting into the business every day.” A Southeast contractor summed up the issue in a succinct manner: “It means more drilling contractors to bid against.”

Complained one Northeast contractor, “Companies are able to purchase used equipment at a fair price, but they really don’t know how to operate the equipment, and then underbid those that do know how to operate equipment properly.” Commented a Midwest contractor, “More companies are getting into the business every day.” A Southeast contractor summed up the issue in a succinct manner: “It means more drilling contractors to bid against.”

When asked what is the biggest challenge facing HDD today, there was no shortage of passionate responses. “Quite simply, design is the biggest challenge we face,” said a Southeast contractor. “Owners do not pay for proper design from the engineers. So engineers push all the design and liability to the HDD contractor – and the contractor accepts it. There needs to be more uniform standards of allocation of HDD risk and liability in the absence of proper design.”

A Texas contractor had distinct opinions on the challenges facing HDD. “Commoditization of the installation method is dropping prices; proper as-built procedures and consistency across all industries is needed; and improper design and inspection of trenchless crossings is a major problem.”

One Southwest contractor made a strong case for sharing risk on HDD projects. “Technology has increased our accuracy to steer and locate pipes and conduit through the sheer amount of utilities that are now present, but the laws and regulations governing utility companies with respect to the tolerance that bores can be off and accountability of not showing up is way behind.

“There needs to be new laws passed to hold utility companies and contract locators fiscally liable for late and missed locates. Contractors pay heavily for hits and the rising cost of insurance – not to mention downtime waiting on past-due locate tickets. There needs to be some consequences for them if they fail on their part,” the contractor concluded.

Market size

While the various primary market segment shares for HDD remain largely constant, predictable trends continue, according to survey information. It’s no surprise that telecom remains the single largest market segment for HDD with a 24.1 percent market share. That is still a noteworthy increase from 2015 when telecom market share was at 22.8 percent. That strong market is not expected to change much for several years.

As mentioned earlier, water has become a steadily increasing partner of HDD applications. In fact, its 19.9 percent market share climbed again from 19.5 percent a year ago. While sewer applications are generally closely linked with water, the nature of gravity sewers requiring tight tolerances continue to be an inhibitor for HDD growth. Maintaining line and grade – while obtainable – still tends to be time-consuming, costly and tedious. The sewer market share is projected to drop from 9.1 percent in 2015 to 7.8 percent in 2016. Indeed, most of the major sewer work performed via HDD is largely limited to interceptor or pressure sewer projects.

As mentioned earlier, water has become a steadily increasing partner of HDD applications. In fact, its 19.9 percent market share climbed again from 19.5 percent a year ago. While sewer applications are generally closely linked with water, the nature of gravity sewers requiring tight tolerances continue to be an inhibitor for HDD growth. Maintaining line and grade – while obtainable – still tends to be time-consuming, costly and tedious. The sewer market share is projected to drop from 9.1 percent in 2015 to 7.8 percent in 2016. Indeed, most of the major sewer work performed via HDD is largely limited to interceptor or pressure sewer projects.

Also remaining a strong market for HDD is gas distribution with a market share of 18 percent. That market segment will probably continue to increase in coming years as new gas installation projects are being launched at a fast pace. Electric transmission and distribution construction may be approaching its peak in the near future but still accounts for 12.8 percent of the market.

The pipeline transmission and gathering market dropped from a 14 percent share in 2015 to a projected 12.1 percent in 2016. That decrease was anticipated as U.S pipeline work will be slowing over the next year.

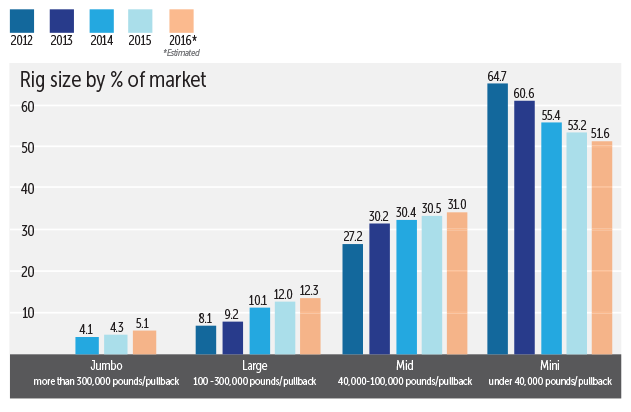

Rigs and age

The size of HDD rigs is generally rated by pounds of pullback force and torque. The 2016 survey again reflected continuation of a trend towards larger rig sizes, whether a contractor is upsizing from a small- to mid-size unit or even to a large or jumbo rig (which generate pullback forces greater than 300,000 pounds). While large and jumbo rig sales will probably start seeing a reduction of sales in 2016 due to the slowdown in energy pipeline work, there has been a steady expansion in applications and needs for larger HDD equipment for several years. Water markets, for example, frequently required large rigs to pull-in large HDPE, cast iron or PVC pipe diameters due to weight issues. Jumbo rig market sales should jump to 5.1 percent of total rig sales in 2016 and large rigs will grow from 12 percent to 12.3 percent.

Mini rugs (under 40,000 pounds of pullback) still dominate the market at a projected market share of 51.6 percent with mid-size rig sales growing to 31 percent.

The overall age of the HDD rig fleet is a good indicator of the economic health and growth of the industry. As more and more contractors have entered the industry or expanded their market presence to meet the demands for booming fiber, gas and energy markets among others, the active rig count has increased and gotten younger.

HDD rigs still in service that are older than 10 years comprise 14 percent of the fleet, a major drop from a year ago (20.3 percent). Rigs 5 to 10 years old comprise 31.9 percent, units only 2 to 5 years old have grown to 31.3 percent and rigs less than two years of age jumped from 18.7 percent in 2015 to 22.8 percent of the market in 2016.

As the HDD market has matured, used and refurbished equipment sales have become big business. In 2016, 56 percent of contractors who plan to add new drilling units will strongly consider purchasing a used rig. The preferred size of used equipment to be considered is evenly split between mini- and mid-sized rigs at 44 percent each.

In 2015, contractors averaged buying about 1.5 units (all size classes) but are expecting to increase that average to almost two rigs per customer (all size classes) in 2016.

High density polyethylene (HDPE) pipe continues to be the number one pipe used for HDD work by a large margin with a 49.9 percent market share. Newer PVC pipe joining methods such as fusible PVC and improved restrained joint technology have made PVC a strong contender in HDD applications as well. It claims a 22.3 percent market share followed by steel pipe at 14.2 percent and ductile iron at 9.1 percent.

Each year, we use the HDD Survey to ask contractors what qualities are most important from their HDD equipment/service providers. The service category, typically the strongest area named by contractors, jumped even more for this report, increasing to 80 percent from 71.4 percent. Service continues to dominate with 71.4 percent of contractors highlighting that quality. Technical knowledge and quality also were cited much more frequently by contractors, both registering at 68 percent of respondents. While cost of equipment remains important, it is notable that it was cited by only 44 percent of survey participants as a major issue in dealing with vendors.

Comments